Socioeconomic Update – April 2026 Volume 1

Inflation Reverses as Energy Shock Reignites Price Pressures

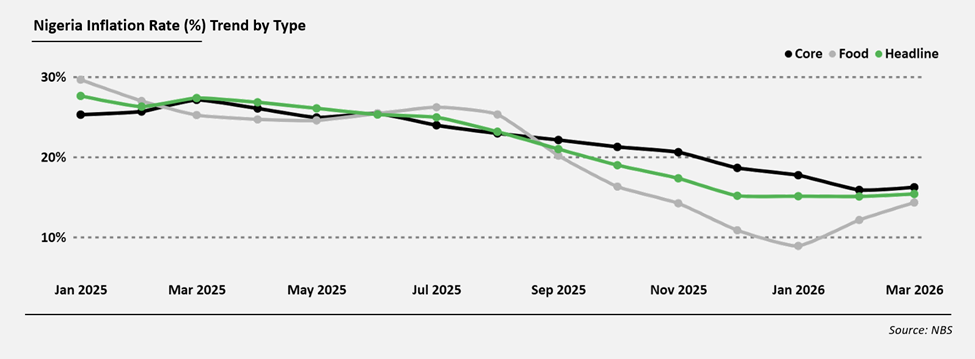

Nigeria’s inflation path reversed in March, with headline inflation rising to 15.38% from 15.06% in February, the first increase in twelve months. More concerning is the sharp acceleration in monthly inflation to 4.18%, up from 2.01%, signaling a rapid and broad-based build-up in price pressures.

The trigger is external, but transmission is domestic. The disruption of the Strait of Hormuz has lifted global oil prices, feeding into Nigeria’s fuel and transport costs. With food and logistics already structurally constrained, the pass-through has been swift and widespread. Food inflation rose from 12.12% in February to 14.31% year-on-year (4.17% m/m), driven by staples, while its contribution to headline inflation remains dominant at 5.55 percentage points.

The escalation of core inflation from 15.88% in February to 16.21% year-on-year, and a significant 4.03% month-on-month surge, highlights the deepening impact of second-round price effects. Price pressures are no longer isolated; they are diffusing across services, with restaurants and accommodation contributing 3.26 ppts and transport 1.80 ppts, marking a shift toward economy-wide inflation.

Spatial dynamics reinforce the structural story. Rural inflation accelerated to 17.22% y/y, with a sharp 6.73% monthly spike, far outpacing urban areas (14.64%). Combined with a rising 12-month average inflation of 20.05%, this suggests persistent medium-term pressure.

For the CBN, this disrupts the easing narrative. With policy rates at 26.5%, a hold is likely as risks tilt upward. The World Bank estimates oil pass-through alone could add ~3.1ppts to inflation, implying further upside. The full effects of the current energy shock are yet to be fully reflected and should become more evident in April, as lagged fuel cost adjustments, transport repricing, and supply chain pass-throughs filter more completely into consumer prices.

Nigeria Crude Production: Opportunity Constrained by Structure

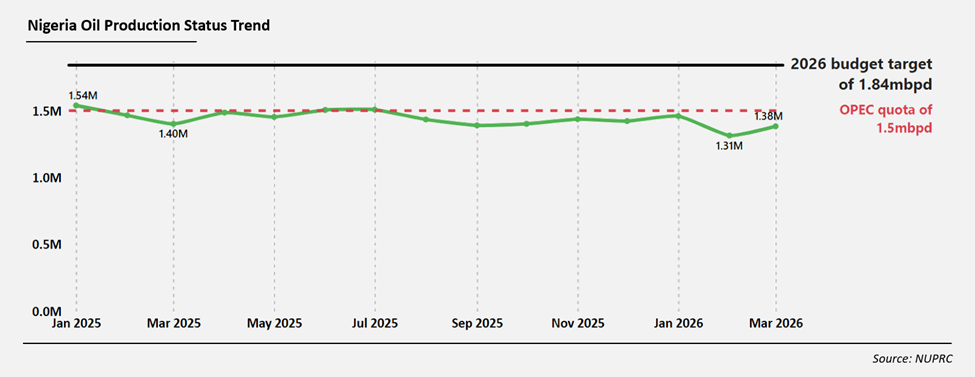

Nigeria’s Q1 production data underscores a widening gap between market opportunity and domestic capacity. Output averaged 1.38 mbpd in March (Jan: 1.46; Feb: 1.31), leaving the country at just 92% of its 1.5 mbpd OPEC quota and significantly below the 1.84 mbpd budget benchmark. This underperformance is occurring at a strategically favourable moment: Brent crude has remained above the $64.85 fiscal benchmark, supported by geopolitical disruptions in the Middle East.

Yet the revenue upside is materially diluted. With approximately 240,000 bpd in encumbered cargoes, effective free production falls to 1.14 mbpd. Applying a 60% government take implies 0.68 mbpd of net fiscal barrels, sharply limiting exposure to elevated spot prices which implies that Nigeria is capturing only a fraction of the current price windfall.

Structural constraints remain binding. Persistent pipeline vandalism, underperforming terminals, and aging infrastructure continue to cap output. The volatility across the quarter, February’s sharp dip and only partial March recovery, reinforces that production instability, not just capacity, is the core issue.

From a fiscal lens, the arithmetic is compelling but conditional. At $90/bbl, incremental revenues could exceed $6bn annually, enough to offset fuel-induced household cost pressures. However, transmission remains uncertain. Without deliberate fiscal discipline, windfalls risk absorption into debt service and recurrent spending.

This account reinforces the historical narrative that Nigeria’s constraint is not price, but production. Until reliability improves, elevated oil markets will continue to translate into missed fiscal opportunity.

Nigeria 2026: Stabilization Gains Meet External Shock

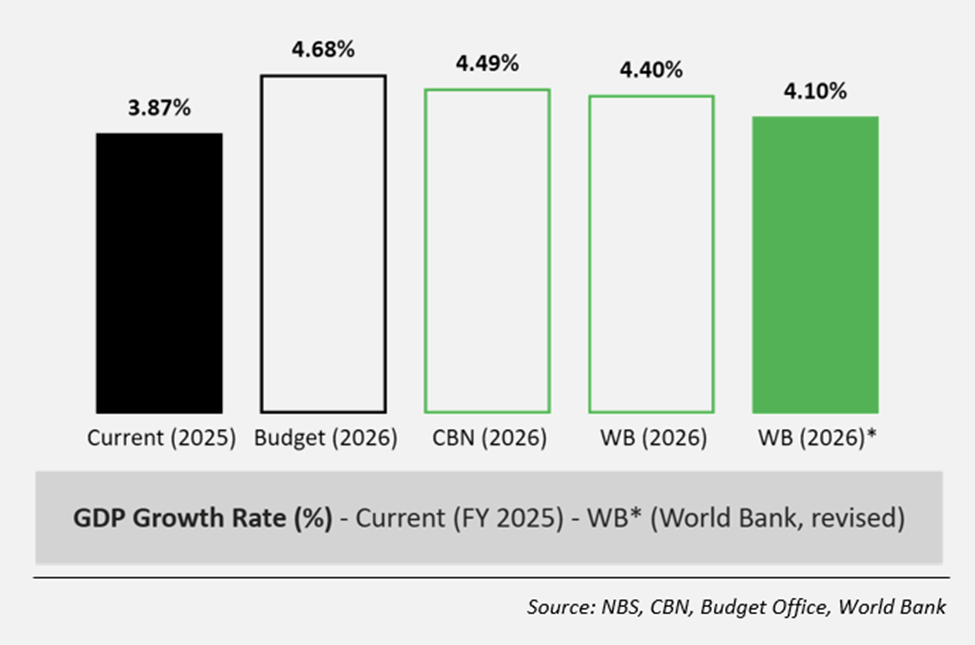

The World Bank has revised its 2026 growth forecast for Nigeria to 4.1 percent, according to its April 2026 Africa Economic Update, down slightly from the 4.4 percent projected in January. The adjustment reflects slower capital accumulation, persistent structural constraints, and the emerging impact of external shocks. In response, the Bank recommends maintaining tight monetary conditions, avoiding broad subsidy restoration, and channeling oil price windfalls into fiscal buffers rather than recurrent spending, and prioritizing macroeconomic credibility over short-term relief.

Investment dynamics continue to shape the outlook. Gross capital formation historically remains low at roughly 13-16 percent of GDP, and private sector investment has shown limited acceleration despite stabilizing macro fundamentals. While services-led sectors such as ICT, finance, and real estate support headline growth, the structural deficit in productive capacity suggests that the 4.1 percent forecast depends heavily on execution and broader confidence measures.

At the same time, Nigeria faces renewed inflationary pressures. Global oil prices, elevated, with recent spikes toward $100 per barrel amid Middle East tensions, transmit into domestic fuel, transport, and food costs. Ongoing FX reforms and enhanced price transparency through EFEMS (Electronic Foreign Exchange Matching System) have moderated pass-through, yet household expenditures remain sensitive to energy and logistics costs. In this context, the World Bank’s approach to saving windfalls and avoiding subsidy expansion aligns with the need to maintain macro stability while navigating these shocks.

Ultimately, Nigeria’s 2026 performance will hinge not only on headline GDP numbers but on whether stabilization efforts translate into tangible improvements for investment, inflation containment, and inclusive growth. Execution discipline and policy calibration remain central to sustaining confidence in the economy.

Nigeria’s ₦4 Trillion Power Bond: Fiscal Risk or Necessary Intervention?

The World Bank, in its latest Nigeria Development Update, flagged Nigeria’s ₦4 trillion power sector bond programme as a material fiscal risk, warning that the initiative converts accumulated electricity sector payables into formal sovereign obligations with sustained claims on federal revenues. The caution warrants examination from two fronts.

The fiscal concern is grounded. The programme settles over ₦6 trillion in generation company receivables, arrears built since 2015 through tariff suppression and payment cascade failures, at an estimated 17-18 percent yield over seven years, meeting international criteria for Public and Publicly Guaranteed debt classification. Against a backdrop of debt service absorbing 50–60 percent of federally retained revenue in 2025, total public debt at ₦153 trillion as of Q3 2025 (DMO), and a projected ₦23 trillion deficit in 2026, additional sovereign obligations carry real crowding risks for capital expenditure and subnational transfers.

The fiscal risk, though, must be weighed against the cost of maintaining the status quo, not in isolation. The World Bank’s estimates put Nigeria’s annual GDP loss from power unreliability at $26–29 billion (8 – 10% of 2025 nominal GDP). The ₦6 trillion in arrears already represents a de facto sovereign liability, formalizing it arguably improves fiscal transparency, a principle the World Bank endorsed in India’s comparable 2015 UDAY scheme, which restructured ₹2.32 trillion in state electricity board debt as a platform for sector reform.

Implementation remains the critical variable. GenCos report zero disbursements despite the ₦501 billion first tranche closing with full subscription in early 2026. Whether the programme becomes reform catalyst or deferred liability ultimately depends on execution discipline.

Nigeria’s FX Stability: Reform Gains Meet External Headwinds

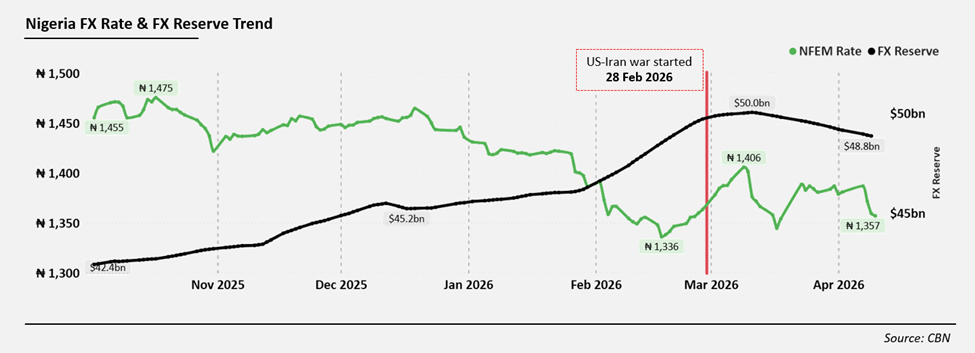

Nigeria’s foreign exchange market, which registered meaningful stability gains through early 2026, is again under pressure as external shocks and softening capital inflows test the durability of CBN-led reforms. The naira weakened to approximately ₦1,386.66 per dollar on early April 2026 from about ₦1,344.42 per dollar in mid-March, while external reserves declined consecutively across sessions to about $48.8 billion in early April following a peak above $50 billion in early March (CBN), a trajectory that warrants careful reading.

The immediate pressure is partly external. Heightened geopolitical risk stemming from US-Iran tensions has triggered a broader risk-off sentiment in global markets, dampening offshore investor appetite for frontier market assets. Portfolio inflows, which surged 151 percent to $1.6 billion in January 2026, have since slowed materially. This slowdown, paired with a $1.2 billion erosion of external reserves from March peak, exposes how sensitively Nigeria’s FX liquidity position responds to shifts in global risk appetite.

The structural vulnerability beneath the headline is well-documented. Nigeria’s FX market remains anchored to short-term portfolio flows and commodity earnings rather than durable export receipts. Non-oil exports reached $6.1 billion in 2025, accounting for only about 15% of Nigeria’s $41.6 billion merchandise import bill (NBS). This leaves an import-financing deficit of about $35.5 billion that must be met through oil receipts, remittances, and capital inflows, more than 80% of which remain short-term and reversible.

CBN reforms, market unification, EFEMS-based price discovery, and BDC reintegration since February 2026, have improved transparency and supported reserves accumulation. They provide the plumbing for stability, but inflow depth determines durability. Until FX inflows broaden beyond yield-seeking capital, external shocks will continue to disproportionately transmit into naira volatility.

Nigeria’s ₦68.3 Trillion Budget: Expanded Ambitions, Familiar Constraints

The National Assembly passed Nigeria’s 2026 Appropriations Act at ₦68.323 trillion on March 31, a ₦9.85 trillion increase over the December submission of ₦58.4 trillion, driven by a ₦9.3 trillion supplementary request to regularize legacy capital projects, plus a further ₦623 billion added by the Senate. The revised budget is benchmarked at $75 per barrel and ₦1,512 per dollar, with total projected revenue of ₦36.863 trillion and a deficit of ₦31.46 trillion, now exceeding 6 percent of GDP and materially above the 3 percent ceiling in the Fiscal Responsibility Act.

The structure warrants scrutiny. Debt servicing at ₦15.809 trillion consumes 23 percent of the approved budget and approximately 46 percent of projected revenue, continuing to crowd out productive expenditure. Capital allocation stands at ₦32.287 trillion but the 2025 precedent is instructive: only ₦834.8 billion, or 7.72 percent of the pro-rata benchmark, was released in the first seven months of that fiscal year. The extension of the 2025 capital budget to June 30, 2026, on the same day the 2026 budget passed, means Nigeria now runs three concurrent fiscal frameworks simultaneously.

The supplementary request was read and approved within hours at the same plenary session without substantive deliberation, a legislative process that offered limited opportunity for scrutiny. This raises questions about whether the expanded envelope reflects genuine project readiness or political accommodation ahead of the 2027 electoral cycle. This is not the first time Nigeria has approved a budget larger than its execution capacity, but the fiscal conditions of 2026 make the execution question more consequential than usual. With debt service at ₦15.8 trillion, a deficit exceeding 6 percent of GDP, and three overlapping budget cycles running concurrently, the margin for further slippage is narrowing. What happens between appropriation and disbursement this year will shape both fiscal credibility and real economic delivery well into the next political cycle.