Socioeconomic Update-May 2026 Volume 1

Reserve Drawdown Enters Sixth Consecutive Week as Inflation Reversal Deepens Macro Pressure

Nigeria’s external reserves shed approximately $855 million across five weeks, falling from $49.18 billion on April 1 to $48.33 billion by May 7, extending the drawdown identified in the April Bi-Weekly update into a fifth consecutive week. A partial recovery $218 million was recorded May 7 to May 14 bringing net drawdown to $637 million. The trajectory marks a material reversal from the $50.08 billion peak of March 12 itself a 17-year high and reflects converging forces tracked consistently across this series: the US-Iran-driven risk-off shift in global capital markets compressing portfolio inflows that had surged 151 percent to $1.6 billion in January; rising import costs from elevated global oil prices and freight rerouting adding dollar demand at the worst possible moment; and a fiscal environment where a budget deficit exceeding six percent of GDP and debt service absorbing an estimated 46 percent of projected federal revenue leave the government structurally unable to absorb external shocks. Fitch Ratings revised its reserves forecast downwards to approximately $47 billion by year-end, consistent with the current drawdown trajectory.

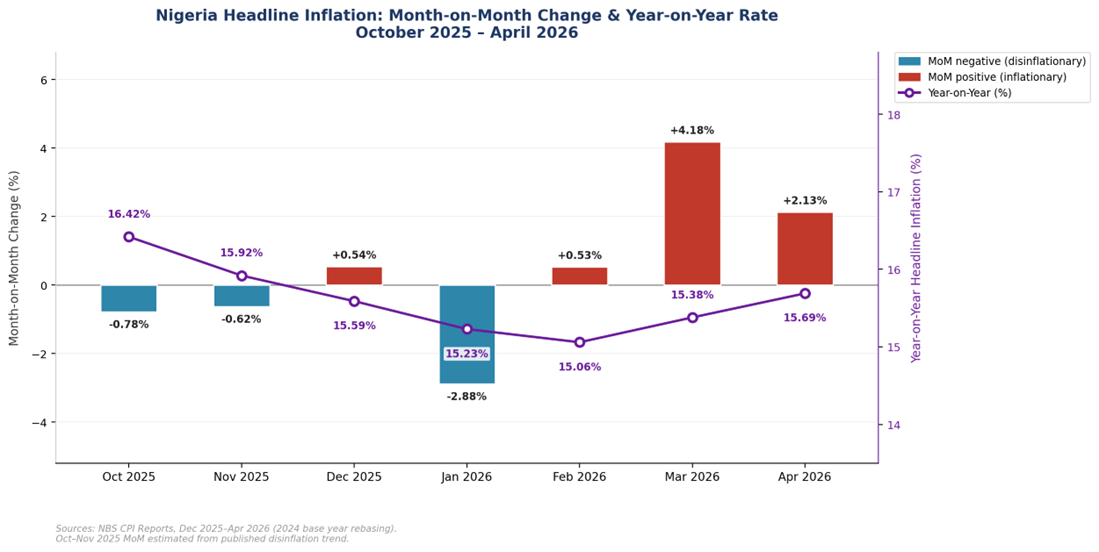

Compounding the external pressure, Nigeria’s headline inflation reversal continues into its third month-on-month increase in April, rising to 15.69 year-on-year from 15.38 in March 2026. Food inflation, comprising 52 percent of the CPI basket, climbed to 16.06 percent year-on-year, up markedly from 14.31 percent in March and now the largest single driver of the headline reading, contributing 6.40 percentage points to the annual figure; monthly food price growth eased slightly to 3.63 percent from 4.17 percent, consistent with the same pattern of a decelerating monthly impulse alongside a still-rising annual rate. Core inflation stood at 15.86 percent year-on-year, with the monthly core rate dropping to 1.03 percent from 4.03 percent in March, a more pronounced deceleration that reflects the fading of the concentrated energy cost shock and some stabilisation in services pricing, even as restaurants and accommodation services continued to contribute 3.56 percentage points and transport 1.70 percentage points to the annual headline. The CBN’s policy rate, reduced 50 basis points to 26.5 percent in February when the disinflation trend appeared intact, now faces a more nuanced hold: the monthly deceleration reduces the immediate pressure for a reactive tightening, but the still-rising annual rate and the food inflation acceleration from 14.31 to 16.06 percent foreclose any prospect of a further cut, leaving producers and businesses in an extended period of elevated credit costs with the earliest plausible easing window pushed into late 2026 at the earliest.

The convergence of an accelerating reserve drawdown with an inflation reversal captures the binding constraint on Nigeria’s macro position. An external buffer being consumed to defend the naira at the same moment that rising consumer prices are squeezing real incomes and limiting the CBN’s room for easing represents simultaneous pressure on stability from both the external and domestic accounts. The reform narrative has rested substantially on rebuilding reserves and reducing inflation; both are now moving in the wrong direction within the same two-month window, and the fiscal environment provides limited counter-cyclical capacity to break the feedback loop without structural intervention.

The government’s response includes a raft of high-calibre appointments confirmed and announced throughout April: Taiwo Oyedele as Finance Minister anchoring fiscal discipline and revenue expansion; Joseph Tegbe as Minister of Power mandated to reduce the energy cost burden that feeds directly into both consumer inflation and producer input costs; Ambassador Enikanolaiye in Foreign Affairs reinforcing the diplomatic architecture for trade and investment partnerships; and the appointment today of Maj. Gen. Adeyinka Fadewa as Special Adviser on Homeland Security to sharpen intelligence-led coordination of the security environment that constrains oil production and disrupts agricultural supply chains. Together, these appointments represent a deliberate attempt to place technically credible leadership across the precise institutional nodes where Nigeria’s macro vulnerabilities are most acute, creating the conditions simultaneously for inflationary constraint, revenue mobilisation, and reduced exposure to the geopolitical shocks that have driven the reserve and inflation dynamics of the past six weeks. Whether those conditions translate into outcomes within the electoral window available depends critically on one sector above all, the regulatory frameworks surrounding the reform of Nigeria’s petroleum sector.

Senate Confirms Rabiu Umar as NMDPRA Chief Executive Amid Fuel Import Licence Controversy

The Senate confirmed Rabiu Abdullahi Umar as NMDPRA Chief Executive on May 7, 2026, the third leadership change at the authority in under a year, following President Tinubu’s nomination on April 29 and the abrupt removal of Saidu Mohammed just four months into his tenure. Two wider headlines shape this announcement: an escalating aviation fuel pricing crisis with jet A1 prices reaching ₦1,760 to ₦1,988 per litre in Lagos alongside a gasoline supply shortage in country and increasing international demand for Nigeria’s fuel production, and the confirmation by a senior petroleum sector official that import licences covering between 600,000 and 720,000 metric tonnes of petroleum products had been issued to fuel marketers in an attempt to guarantee oil supplies and limit inflationary pressures. At his Senate screening on May 5, Umar framed his mandate in terms that directly acknowledged the need to adapt regulation to the domestic supply requirements of the country. His election

“Global events may affect prices, but they should not define Nigeria’s stability. Our task is to build a petroleum system strong enough to absorb shocks, protect supply, and keep homes, industries, and transport moving in every season.” — Rabiu Abdullahi Umar, NMDPRA Senate Screening, Abuja, 5 May 2026

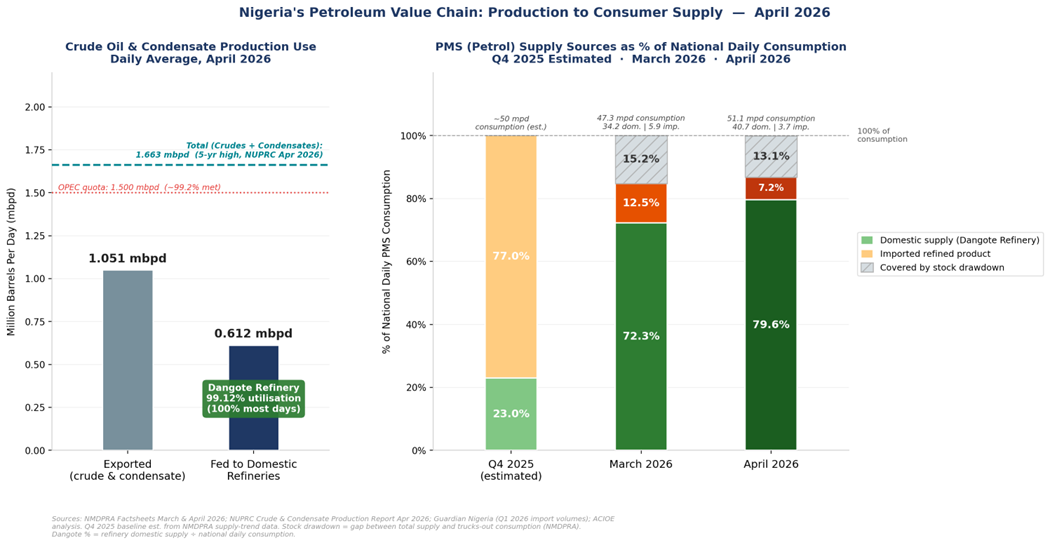

The import licence disclosure reignited the structural dispute between Dangote Petroleum Refinery and successive NMDPRA leaderships. Dangote has consistently argued that licenses issued to marketers directly undermine the commercial viability of the $20 billion domestic refining investment at a time when the refinery is producing PMS, diesel, and aviation fuel for the domestic market, how it appears that the current regulatory position leans towards the assumption that single-supplier dominance creates monopolistic pricing risk requiring competitive imports. In spite of increasing oil premiums and the oil windfall upside potential from increasing domestic production, the Government is demonstrating only a partial capability to sustain its net oil exporter status, as oil imports are still necessary to build buffers amidst global market volatility. The leadership change therefore oversees an expected period of aggressive import substitution to increase domestic supply using local refineries: April 2026 highlighted three records – domestic oil production, Dangote Oil Refinery output optimisation, and record supply of refined Dangote petrol to the domestic market (~79%). This structural shift, see illustration 2, demonstrates a marginal buffer improvement mitigating global oil price shocks into domestic consumer prices, FX demand, and downstream sectors across the economy.

Increasing domestic supply of oil refined oil benefits from Dangote Refinery optimisation, whilst limited oil supply (~18 days PMS Stock Sufficiency) remains a key sector and inflationary challenge.

Umar’s appointment, drawing on seven years as Group Chief Commercial Officer at Dangote Industries through the refinery’s commissioning phase, preceded by operational roles at Oando Terminals and Logistics and energy strategy positions at Lafarge Africa across West Africa, positions him to attempt significant regulatory intervention, aimed at guaranteeing energy security, regulatory efficiency to guarantee domestic refinery capacity, and increasing fuel supply. His experience places him uniquely able to navigate industry ramp-ups, domestic private sector regulatory implementation, and the disinflationary demands required to boost general economic growth. The structural significance extends beyond the petroleum sector: every cargo of imported refined product simultaneously creates FX demand that compounds the reserve drawdown, adds to transport and logistics costs, and generates an inflationary impulse that monetary policy cannot efficiently target. This adds to strained fiscal capacity as electoral spending expectations grow into the 2027 election cycle and Government spending challenges, across health, defence, and infrastructure meet politically sensitive civil society demand.

Government Reorganises Its Security and Diplomatic Architecture Ahead of the 2027 Electoral Cycle

The appointment of Major General Adeyinka Fadewa (Rtd) as Special Adviser on Homeland Security, announced May 11, adds the final piece to a concentrated week of senior government appointments that collectively represent the most visible reorganisation of Nigeria’s executive architecture since the 2026 budget was signed into law. Fadewa, a decorated 30-year veteran of military intelligence who spearheaded the creation of Nigeria’s Intelligence Fusion Centre at the Office of the National Security Adviser between 2015 and 2021, integrating the DIA, NIA, DSS, Police, and Armed Forces into a single national threat assessment platform, joins Ambassador Enikanolaiye in Foreign Affairs, Tegbe in Power, Oyedele in Finance, and Umar at the NMDPRA in an institutional construct the Presidency describes as strengthening internal security coordination, enhancing intelligence-driven operations, and deepening inter-agency collaboration against emerging threats.

The political context continues to increase in relevance to wider regulatory changes: with the 2027 general elections approaching and INEC having submitted a ₦873.78 billion election budget to the National Assembly — a 145 percent increase from 2023 — the government is constructing an institutional narrative of competence, security, and stability that is as much electorally motivated as it is operationally necessary. Fadewa’s mandate to sharpen intelligence coordination is directly relevant to pipeline security and political stability both adding constraints to Nigeria’s crude production below OPEC quota, the shortfall that has compressed FX inflows and contributed to the reserve drawdown. Enikanolaiye’s diplomatic remit matters to the bilateral energy investment discussions through which Nigeria is attempting to convert its current Bonny Light premium into durable upstream capital commitments. Whilst the broader security environment, including banditry constraining agricultural supply in the North-West and insurgency disrupting the North-East food belt, continues to act as a structural component of food, transport, and energy inflation which is seeing the CPI reversal.

The regulatory pressures are therefore heading into a critical period of expected changes in Q2 bringing into maturity frameworks to address inflation, increase FX reserve share, and build sector resilience from geopolitical shocks. The government’s ability to stabilise its macro position before the 2027 electoral cycle compresses its reform window and adds pressure to its policy execution: fiscal discipline to contain the reserve drain, power sector improvement to reduce the energy cost pressure embedded in every inflation reading, petroleum supply regulation to moderate fuel price pass-through, and security coordination to address the constraints on oil production and agricultural output that make Nigeria’s vulnerability to geopolitical shocks structural rather than cyclical. Changing appointments will also challenge policy execution stability, with delays to implementation possible. A raft of appointment changes are expected to continue throughout Q2. These regulatory changes also signal increasing opportunities for private sector contributions to long term stability with the Nigerian government signaling ongoing import dependency alongside a transition to domestic resilience.