Socioeconomic Update-April 2026 Volume 2

Nigeria’s 4Ps Model: From Reform Announcement to Execution Accountability

Taiwo Oyedele’s appointment as Finance Minister following the resignation of Mr. Wale Edun is a consequential personnel decision. His leadership of the Presidential Fiscal Policy and Tax Reform Committee, built on a PwC career focused on tax architecture, gives him genuine reform credibility.

However, the fiscal position he inherits is structurally stressed. Debt service stands at an average of ₦1.3 trillion per month, against a federal FAAC receipt last month of slightly over ₦700 billion, the government is spending more servicing debt than it is collecting in revenue share. Capital expenditure has borne the consequence, and the development spending underpinning the reform narrative is not happening at scale. The revenue imperative is beyond dispute; the how remains the challenge. Two levers are available: oil production recovery, which is partly outside the ministry’s direct control, and tax base expansion into the informal economy, where Oyedele’s prior reform work is directly relevant. Neither delivers quickly.

His 4Ps public-private partnership framework is a reasonable reframing of the government-private sector relationship, and the underlying diagnosis, that macroeconomic stability and firm-level operating conditions remain decoupled, is accurate. But Nigeria has a long history of well-designed frameworks and weak execution, and the 2027 electoral cycle creates a structural headwind to the policy consistency the model requires. Strong execution by the Minister will be critical in order to address the fiscal challenge.

Nigeria’s 2026 Tariff Reforms: Lower Import Costs, Higher Consumption Taxes

The Federal Government introduced its 2026 Fiscal Policy Measures on April 1, cutting import duties on a wide range of goods while introducing new consumption taxes. Machinery and equipment for agriculture, manufacturing, power, and mining now attract zero duty, directly lowering the cost of productive investment. Key food staples also record meaningful reductions: rice duties fall from 70% to 47.5%, crude palm oil from 35% to 28.75%, and raw cane sugar from 70% to 55%. Passenger vehicles drop from 70% to 40%, and pasta moves from outright import prohibition to a 30% tariff, opening a previously closed category. For manufacturers who depend heavily on imported inputs, the measures reduce operating costs and improve the economics of local production at a time when margins have been under sustained pressure. Running alongside the duty cuts, new excise taxes take effect from July 2026 on beer, non-alcoholic beverages, tobacco, and private vehicles with engines above 2,000cc, with rates set to increase each year through 2028, reaching their highest point in an election year. The structure is deliberate: the government is easing the cost of production while raising revenue from consumption. The risk is that the external environment has narrowed the window for these reforms to work as intended. Fuel costs have risen sharply, fertiliser supply routes have been disrupted, and freight costs have risen as cargo reroutes around the Cape of Good Hope, pressures that collectively outweigh the price relief the tariff reductions were designed to deliver. The reforms point in the right direction, but their impact will depend heavily on whether the external environment stabilises and whether the government holds the line when the political cost of doing so rises.

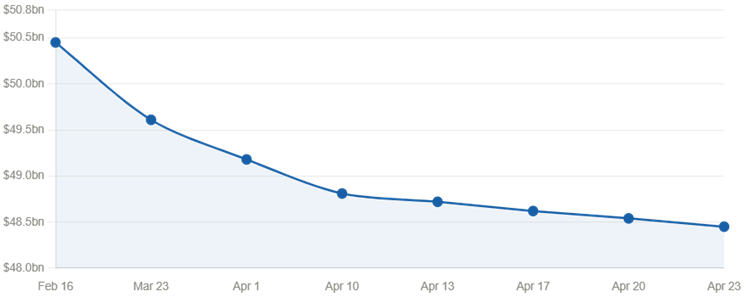

Nigeria’s External Reserves Decline $731 Million in April

Nigeria’s external reserves fell by approximately $731 million in the first three weeks of April, dropping from $49.18 billion on April 1 to $48.45 billion as of April 23, according to Central Bank of Nigeria data. The decline extends a drawdown that began in March, when reserves slipped from a peak of $50.08 billion, reversing the upward trend that had carried gross reserves to their highest level since 2013 earlier in the year.

The pressure reflects two converging forces. The CBN has been actively deploying foreign exchange to defend the naira and maintain market liquidity, a posture made more urgent by FX inflows falling to a 16-month low of $2 billion, alongside elevated debt service obligations. At the same time, foreign portfolio inflows — which surged by 151 percent to $1.6 billion in January — have slowed materially. Geopolitical tensions stemming from the US-Iran standoff have triggered a broader risk-off shift in global markets, raising the cost of retaining yield-seeking capital that had driven Nigeria’s earlier reserve build-up and prompting investors to reduce exposure to frontier and emerging market assets in favour of safer alternatives.

At the IMF/World Bank Spring Meetings in Washington, CBN Governor Olayemi Cardoso characterised the movements as routine, noting that reserves still cover approximately 13 months of imports, well above the threshold recommended by international financial institutions, and that Nigeria’s FX market is now more liquid and market-driven than in prior years. The reassurance is not unfounded as the current reserve level remains significantly stronger than the roughly $32 billion recorded at the same point last yearz, and Brent crude trading well above the budget benchmark of $64.85 per barrel continues to support oil inflows.

The concern is not that reserves will run out, but that the current direction of drawdown, if sustained, narrows the buffer that took two years of reform to build. A market where the CBN is doing increasing work to hold the exchange rate steady, while inflows soften, is one where that buffer is being spent rather than replenished. How long that remains manageable depends on how the geopolitical situation resolves and whether inflows recover meaningfully before the pressure compounds.

Nigerian Crude Commands Highest Price Premium in Three Years

Nigerian crude grades are attracting their strongest market premiums in at least three years for May 2026, according to the NUPRC’s April fiscal oil price schedule. Bonny Light’s differential against Dated Brent jumped to +$5.66 per barrel in May, from +$0.43 in March. Deepwater grades moved even more sharply, with Egina rising to +$8.70 and Bonga to +$7.55. Several grades that spent much of the first quarter in negative territory have fully reversed, with Akpo swinging from -$0.30 in January to +$5.19 in May.

The shift reflects genuine demand. Atlantic Basin refiners have been actively replacing Persian Gulf supply disrupted by the US-Iran tensions, and Nigerian crude, being predominantly light and low-sulphur, is exactly what those refiners need. With Brent trading around $106 per barrel, well above the $64.85 budget benchmark, Nigerian grades are realising close to $112 per barrel on May liftings.

For government revenue, the timing is favourable. Higher realised prices directly improve royalty and tax receipts on each barrel the federation captures. At current price levels, the monthly uplift above budget assumptions could reach between $370 and $494 million.

The constraint, however, remains production. Nigeria is producing approximately 1.38 million barrels per day excluding condensates, still below its 1.5-million-barrel OPEC quota and well short of the 1.84 million barrels assumed in the 2026 budget. The premium is real, but fewer barrels than budgeted means the revenue upside is only partially realised. Until output catches up, strong prices will continue to cushion but not fully compensate for the production gap.