Socioeconomic Update- March 2026 Volume 2

Headline Inflation Edges Down as Monthly Price Pressures Reverse

Nigeria’s headline inflation edged down slightly to 15.06% in February from 15.10% in January, marking eleven straight months of year-on-year disinflation. On the surface, that looks like continued progress. Beneath it, the picture is more concerning.

The monthly trend reversed sharply. Month-on-month inflation jumped to +2.01% in February after falling 2.88% in January, a significant swing driven by both food and core prices moving higher together. That breadth matters: it signals broader price pressure, not a one-off spike.

Food prices are the main driver. Month-on-month food inflation surged to +4.69% (from -6.02% in January), pushing the annual food inflation rate to 12.12%. Staples like beans, yam flour, millet, and cassava saw notable price increases. The causes are structural: insecurity in farming regions is disrupting supply, logistics costs remain high, and the seasonal shift toward planting season has tightened market stocks.

March looks riskier still. Petrol prices have climbed above ₦1,300 per litre following rising global oil prices — Brent crude has crossed $100/barrel amid US-Iran tensions. Higher fuel costs raise transportation and logistics expenses across the economy, which typically feeds through quickly into food and goods prices.

The Central Bank of Nigeria has begun an easing cycle, but the combination of fuel cost pass-through, tight food supply, and seasonal demand could complicate that path. From May onward, election-related spending historically adds further demand pressure making the inflation calculus harder, not easier.

The year-on-year trend remains positive, but February’s monthly data is a clear warning sign. Businesses and investors should expect inflation to remain volatile through mid-year, with upside risk outweighing downside.

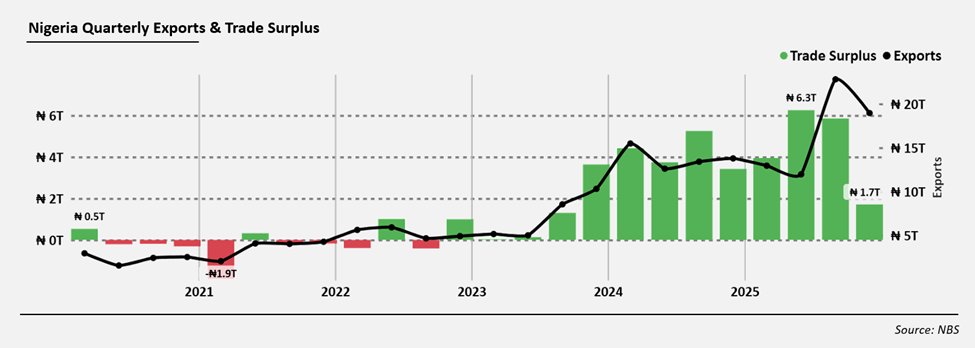

Nigeria’s Trade Surplus Narrows in Q4 2025 as Crude Oil Exports Decline

Nigeria recorded a merchandise trade surplus of ₦1.71 trillion in the fourth quarter of 2025, with exports of ₦18.96 trillion outpacing imports of ₦17.25 trillion. For the full year, the surplus reached ₦17.78 trillion, underpinned by total exports of ₦85.13 trillion against imports of ₦67.35 trillion. Q4 was the softest quarter of the year, with total trade declining 16.88 percent from Q3 2025 and exports falling 5.25 percent year-on-year.

The Q4 decline was concentrated in crude oil, where exports fell to ₦9.70 trillion, down 24.24 percent from Q3 and 29.60 percent year-on-year, accounting for 51.17 percent of total exports. Non-oil exports contributed ₦3.15 trillion, led by agricultural products at ₦1.32 trillion, primarily cocoa beans and sesame seeds shipped to the Netherlands, Belgium, China, and India. Raw material exports, anchored by urea to Brazil, added ₦1.19 trillion, while solid mineral exports reached ₦116.84 billion, up 92.48 percent year-on-year.

Measured in dollars, total exports grew 7 percent year-on-year to $13.21 billion in Q4, while non-oil exports rose 25 percent to $2.19 billion from $1.75 billion a year earlier. For the full year, non-oil exports reached ₦12.36 trillion ($8.60 billion), up from ₦9.09 trillion ($5.94 billion) in 2024. On the import side, China remained the dominant supplier at ₦5.39 trillion, representing 31.22 percent of Q4 imports, followed by the United States at ₦1.61 trillion and the Netherlands at ₦1.52 trillion. Key commodities included motor spirit, durum wheat, crude petroleum, cane sugar, and used diesel vehicles.

The full-year trade balance remained positive, but Q4 reflects the continued structural weight of crude oil in Nigeria’s export mix, with non-oil goods accounting for just 16.59 percent of total exports in the quarter. Sustained improvement in the trade position will depend on improved production output and the pace at which non-oil exports broaden in volume, variety, and sectoral depth.

PSC Profit Oil Remittance to Federation Account Surges Following Executive Order, but Production Gap Persists

The Federation Account received its first full remittance of Production Sharing Contract profit oil in February 2026, following President Tinubu’s Executive Order 9, which ended an arrangement under which only 40 percent of PSC profit oil reached the Federation Account, with NNPC previously retaining a 30 percent management fee and directing a further 30 percent to the Frontier Exploration Fund before any transfer occurred.

The immediate fiscal impact was significant, with NNPC remitting ₦121.34 billion in February under the new framework, more than seven times the ₦16.07 billion recorded in January, bringing the year-to-date PSC remittance to ₦137.41 billion, though the two-month outturn still fell materially short of projections. Against a budgeted ₦394.73 billion for the period, the shortfall on PSC revenue alone reached ₦257.32 billion, and the absence of any interim NNPC dividend in either January or February, despite ₦542.37 billion being projected across both months, meant that these two gaps together account for the bulk of the shortfall against the ₦937.10 billion in oil and gas revenue budgeted for the first two months of the year.

The executive order has improved the remittance architecture and ensures that a greater share of what is produced reaches the public purse, but the net fiscal gain to the Federation is likely to be materially lower than the gross remittance figures suggest. The retained funds previously financed NNPC’s operational costs, frontier exploration activities, PSC monitoring across contract sites, and scheduled repayments on crude-backed loan obligations, including approximately $3.175 billion in facilities secured in 2023, all of which now fall to the government to fund through the budget. Once those costs are absorbed, the effective addition to distributable revenue may amount to between 30 and 40 percent of gross inflows.

Nigeria’s Crude Oil Production Falls to 1.31 Million Barrels Per Day in February 2026

Nigeria’s crude oil production declined to 1.314 million barrels per day in February 2026, a 10.69 percent drop from 1.459 million barrels per day in January, according to direct communication data published in OPEC’s monthly report. The figures exclude condensates, in line with OPEC’s reporting methodology. The decline was partly attributable to the scheduled maintenance shutdown of Shell’s Bonga FPSO facility, which went offline from February 1 with a processing capacity of 225,000 barrels per day and was expected to resume in March.

The February figure leaves Nigeria approximately 186,000 barrels per day below its OPEC quota of 1.5 million barrels per day, extending the country’s run of consecutive monthly quota misses. The shortfall carries a heightened cost in the current price environment. With Brent trading above $100 per barrel in early March and well above the $64 budget benchmark, each barrel not produced represents a more consequential revenue loss than it would under softer price conditions.

The government has approved a fiscal incentive package clearing the path for the Final Investment Decision on the Bonga Southwest Aparo deepwater project. The project involves NNPC Limited and Shell’s SNEPCo among other partners, with projected output of approximately 150,000 barrels per day and an estimated capital commitment of $20 billion. The FID has not yet been taken, but the approved fiscal terms resolve tax and PSC concerns that had stalled the project for nearly seventeen years. If partners proceed, Bonga Southwest Aparo would represent Nigeria’s first deepwater FID since 2008 and a meaningful step toward rebuilding long-term production capacity.

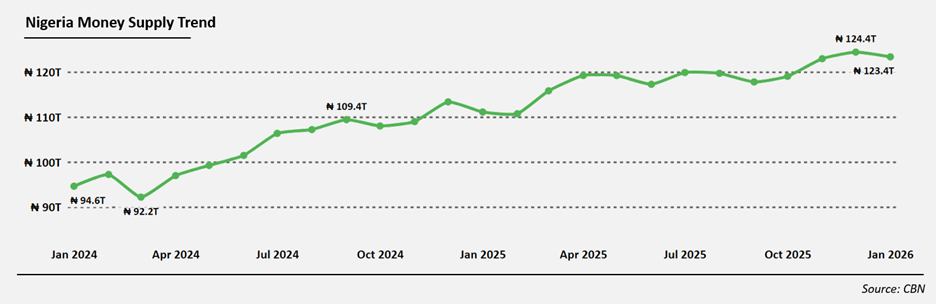

Money Supply Contracts in January as CBN Tightens Liquidity Grip

Nigeria’s broad money supply contracted to ₦123.36 trillion in January 2026, down from ₦124.41 trillion in December, its lowest level in four months and the first monthly decline since September 2025. The drop is not accidental; it reflects a deliberate push by the Central Bank of Nigeria to drain liquidity from the financial system.

The CBN is pulling hard on the brakes. The primary tool has been Open Market Operations — the CBN issued ₦8.53 trillion in short-term bills in January alone, compared to just ₦500 billion in the same month last year. That is a 1,600% year-on-year increase, an extraordinary escalation that has visibly reduced the volume of cash in circulation, which fell 3.66% month-on-month to ₦5.21 trillion.

Credit is tightening across the board. Private sector credit fell to ₦75.24 trillion, with annual growth of just 2.76%, a sharp compression for an economy that historically relied on credit expansion. Government borrowing also edged lower. Lending conditions are tight, and businesses are feeling it.

In late February, the Monetary Policy Committee reduced the benchmark rate by 50 basis points to 26.50% — its first cut in the current cycle — citing eleven consecutive months of easing inflation. The signal is that borrowing costs are beginning to turn.

The apparent contradiction is intentional. Cutting rates while simultaneously draining liquidity is a calibrated strategy: ease the price of money gradually, but keep the quantity under control. Loosening both levers at once risks reigniting the inflation and currency pressures the CBN spent the past year suppressing and it is clearly not ready to take that chance.

The rate cut is a cautious first step toward easing, not a pivot. Liquidity remains tight, credit is constrained, and the CBN is managing the transition carefully.

For businesses, any easing in borrowing conditions is likely to be gradual rather than immediate.