Socioeconomic Update May 2026 Volume 2

Tinubu’s Nairobi Debt Call and the $1.25 Billion World Bank Negotiation Signal a New Phase in Nigeria’s Development Finance Strategy

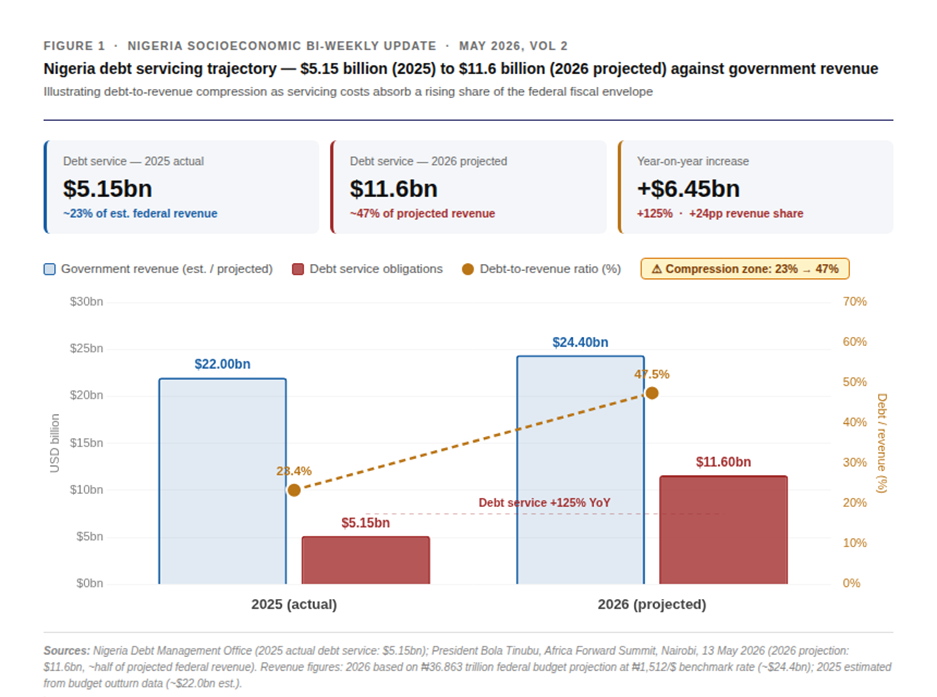

Nigeria’s macro fiscal position moved to the centre of international attention in the second week of May as President Bola Tinubu used the Africa Forward Summit in Nairobi on May 13 to disclose that the country will spend an estimated $11.6 billion servicing its debt obligations in 2026, equating to nearly half of projected government revenue for the year. The trajectory is a consequence of the borrowing acceleration that has accompanied Nigeria’s reform programme, with the World Bank alone having approved approximately $9.35 billion in loans and credits for Nigeria under the current administration between June 2023 and May 2026. Tinubu called directly for a structural overhaul of the international financial architecture, arguing that African sovereigns are systematically treated as permanent high-risk borrowers regardless of fiscal performance or reform delivery: “Our industrial base is being starved of the blood it needs — long-term, affordable finance — while creditors and rating agencies treat African sovereigns as permanent high-risk borrowers, regardless of our fiscal performance.” The framing reflects recent socioeconomic reform packages including fuel subsidy removal, currency unification, and the tax system overhaul. The political timing is compounded by the electoral cycle and ongoing negotiations for a further $1.25 billion World Bank facility, titled Nigeria Actions for Investment and Jobs Acceleration, expected for Board consideration on June 26, 2026, raising total World Bank commitments under the current administration to approximately $10.6 billion.

“Every single dollar that leaves our treasury to pay punitive interest rates is a dollar that did not go into our steel sector, our textile mills, our agro-processed, or our digital industries.” – President Bola Ahmed Tinubu, Africa Forward Summit, Nairobi, 13 May 2026

The proposed $1.25 billion facility would rank as Nigeria’s second largest single World Bank loan under the current administration, covering electricity expansion, digital infrastructure, agriculture, and job creation — sectors that align directly with the disinflationary and FX-generation objectives that the May Bi-Weekly Volume 1 identified as the core policy imperatives for 2026. The Nigerian Economic Summit Group’s (NESG) May 2026 Debt Burden Monitor placed Nigeria’s Debt Burden Index within an upwards trajectory through end of 2025 to the 2023 all-time-high of 83.6. The NESG Debt Burden Index aggregates structural data including external debt-to-exports and debt service-to-revenue to assess and embed structural economic vulnerabilities into an index tracking impact of debt on the economy. As export revenues from oil windfall do not translate into increased state revenues, downstream sectors continue to absorb the inflationary pressures whilst reliance on external borrowing continues. Fiscal pressures are characterised by the Debt Burden Index as “elevated when assessed through a more comprehensive lens”, a qualification that frames the reserve drawdown and inflation reversal trends tracked in volume 1.

For development organisations/partners, the Nairobi engagement signals that Nigeria is actively constructing a multilateral narrative that positions its reform programme as deserving preferential financing terms, a posture that will shape the terms of both the $1.25 billion World Bank facility and the broader borrowing programme. The ₦29 trillion new borrowing envelope built into the 2026 budget signals that multilateral and bilateral partners will remain Nigeria’s primary capital source through the 2027 electoral cycle, creating consistent demand for concessional facilities and reinforcing the leverage development partners hold over policy conditionalities in energy, digital, and health reform.

CBN prepares for June Launch of Digital Payments System Vision, with acceleration of Digital Payment Regulatory Architecture

The two weeks commencing 11 and 18 May highlighted three distinct regulatory streams: central bank identity security rules, sector-wide cybersecurity compliance requirements, and National Assembly legislative progress. This reaccelerates the digital payment regulatory calendar building on the Federal Competition and Consumer Protection Commission’s (FCCPC) Digital, Electronic, Online, or Non-Traditional (DEON) Lending Regulations in 2025 came into force in 2025. The effect for fintech operators, payment service providers, and digital banks is a compliance environment with simultaneous obligations across identity verification, cybersecurity self-assessment, and anticipatory engagement with an emerging statutory framework that would, if enacted, fundamentally restructure how sector oversight is organised.

The first of these policies is already in effect (1 May), with the CBN’s directive limiting the updating of the phone number linked to a Bank Verification Number to once in a lifetime. The measure, issued in late April following growing alarm over SIM-swap fraud, immediately affects the 68.59 million BVN enrolled customers as of May 2026 and every fintech and bank that uses mobile number-linked authentication as a transaction security layer. Simultaneously, the CBN adjusted the official ATM card issuance fee to N1,500 effective 1 May, and mandated personalised transaction limits, allowing customers to set individual spending ceilings below regulatory maximums. For financial services, these changes demand a changing and responsive compliance function, with coordinated adjustments to customer onboarding workflows, fraud alert systems, and terms of service disclosures by the end of May.

Running in parallel was the closing deadline of the CBN’s mandatory Cybersecurity Self-Assessment Tool (CSAT), introduced on 31 March. Deposit Money Banks were given three weeks to submit; payment service providers, microfinance banks, and fintech firms were given five weeks, placing their deadline in the first week of May. The CSAT operationalises a trend tracked across our Bi-Weekly Updates in 2026: the CBN’s systematic extension of cybersecurity compliance obligations from Tier 1 banks outward to the full regulated perimeter. The self-assessment is submitted through a dedicated regulatory portal, and the CBN has indicated it will use results to calibrate supervisory intensity: operators with weak CSAT scores face heightened examination risk in Q3 2026. For Fintech leaders without established compliance teams, the CSAT submission window that closed in early May represents the first structured cybersecurity dialogue with the regulator, creating both exposure risk and opportunity to demonstrate institutional readiness.

At the legislative level, the Nigerian Fintech Regulatory Commission Bill (HB.2389), sponsored by Hon. Fuad Kayode Laguda, continues its progress through the House of Representatives following its October 2025 second reading. The bill proposes establishing a single dedicated statutory body to consolidate oversight currently distributed across the CBN (payments and banking), the SEC (capital markets and virtual assets), NITDA (data and digital economy), and the FCCPC (consumer protection in digital lending). The bill’s legislative trajectory features as part of the broader Q2 2026 regulatory maturation cycle. The bill will structurally change Nigeria’s fintech regulatory architecture since the NDPA, with significant implications for dual-licensed operators and cross-sector payment platforms that currently navigate multiple approval processes averaging 12 months per licence pathway.

The NIBSS New Payment System (NPS), which recorded its inaugural live transaction in 2025, continues its phased rollout as a strategic replacement for the current NIBSS Instant Payment (NIP) scheme. The NPS represents a structural shift toward unified, interoperable, and resilient national payments infrastructure. The NPS trajectory signals a regulatory preference for shared infrastructure over bespoke payment rails, with greater emphasis on interoperability and regulatory visibility as conditions for operating within Nigeria’s payment ecosystem as it scales toward the 11 billion annual transaction volume recorded on NIP in 2024.

APC Primary Victory Consolidates 2027 Electoral Architecture as Opposition Fragmentation Deepens and Health Sector Reform Faces Professional and Legal Resistance

The formalisation of President Tinubu’s status as the APC’s 2027 presidential candidate, confirmed at the APC primaries 25 May, marks the completion of the ruling party’s internal electoral architecture. The primaries produced an overwhelming landslide victory nationally, consistent with Tinubu’s systematic control of APC state structures across 23 of Nigeria’s 36 states. In accepting the APC flag and Certificate of Return, Tinubu framed re-election as a mandate to consolidate and extend the reform agenda, stating: “We will not allow any opposition with no clear vision take Nigeria backward.”

The clarity of the incumbent’s position stands in sharp contrast to a fragmented opposition landscape that remains the defining feature of Nigeria’s 2027 political risk profile. The People’s Democratic Party continues to fracture along factional lines, with Senator Nyesom Wike’s alignment with the Federal Government effectively splitting its national coordination capacity. The African Democratic Congress (ADC) has emerged as an aggregator of high-profile opposition defectors, including former Vice President Atiku Abubakar, former Governors Tambuwal and Lamido, and former Minister Rotimi Amaechi, but its national structure remains underdeveloped relative to the APC’s incumbency machine. Labour Party’s Peter Obi and Rabiu Kwankwaso of the Nigeria Democratic Congress (NDC) represent a separate anti-APC axis capable of delivering targeted South-East and Northern minority votes.

The political stability is further complicated by tension within APC’s own governors’ coalition. Reports in the second week of May identified an aborted move by a faction of APC governors to remove the Progressive Governors’ Forum Chairman, Imo State Governor Hope Uzodimma. The potential destabilisation of the inter-state coordination mechanism that Tinubu’s political strategy relies on for nationwide implementation of the Renewed Hope Agenda faces increasing challenges from domestic fiscal challenges and civic frustration. Tinubu’s intervention also highlights an accelerating risk in policy execution as the electoral cycle pre-empts significant and regular changes in political and ministerial personnel.

The political economy of these concurrent reform streams, (fiscal consolidation under electoral pressure, digital payment regulation intensifying compliance obligations, and health sector reform facing professional pushback) is therefore an ongoing constraint and risk factor: the government’s reform execution capacity is being tested across multiple sectors as the electoral cycle is beginning to compress the reform window. The appointment of a technical leadership cohort across Finance, Power, Foreign Affairs, Petroleum, and Homeland Security will form an active component in delivering measurable outcomes across all five domains. Changing political appointments therefore will continue to punctuate the election cycle and hinder policy execution.

Regulatory Updates to Watch:

- HB.2389 | Fintech Regulatory Commission Bill: House of Representatives — Post-Second Reading. Committee stage. Awaiting report. Sponsor: Hon. F.K. Laguda (Lagos). Status: Active — Q2 enactment window possible.

- CBN Circular | BVN Phone Update Restriction: Effective 1 May 2026. Lifetime limit on mobile number updates linked to BVN. Immediate compliance obligation for all DMBs, PSBs, and fintech operators. Enrolment base: 68.59m (March 2026).

- CBN Directive | CSAT Compliance Deadline: Fintech / PSP / MFB submission window closed approximately 5 May 2026 (five weeks from 31 March). Supervisory review of results expected Q3 2026.

- National Digital Economy & E-Governance Bill: Q2 2026 enactment anticipated. Positions NITDA as a ‘super-regulator’ for digital economy including AI risk classification. Expected to consolidate competing AI-specific bills.