January 2026 Socio-Economic Update Vol 2

IMF Projects Nigeria’s GDP Growth at 4.4% in 2026

The International Monetary Fund projects Nigeria’s real GDP growth at 4.4 percent in 2026, a modest acceleration from its estimated 2025 outcome. The projection reflects expectations of continued macroeconomic stabilisation, gradual reform transmission, and steady expansion in services-driven activity, rather than a sharp cyclical rebound. At the global level, the IMF forecasts growth of about 3.3 percent in 2026, placing Nigeria’s outlook above the world average but broadly in line with Sub-Saharan Africa’s projected recovery which has been estimated at 4.6 percent in 2026.

Nigeria Signs Comprehensive Economic Partnership Agreement (CEPA) with UAE

Nigeria has signed a Comprehensive Economic Partnership Agreement (CEPA) with the United Arab Emirates, deepening bilateral trade and investment ties and establishing a structured framework for goods, services, and capital flows. The agreement comes against the backdrop of a growing Nigeria–UAE trade relationship, with bilateral trade exceeding $4.3 billion in 2024, and reflects Nigeria’s broader efforts to diversify trade partners and reduce reliance on hydrocarbons.

From a macroeconomic perspective, CEPA strengthens Nigeria’s external position by expanding market access for non-oil exports and improving the attractiveness of the country to long-term investment in logistics, energy, and manufacturing. However, its short-term effect on trade balances will depend on how quickly domestic producers can scale output and meet export standards, as tariff liberalisation also raises the risk of higher imports. The agreement therefore shifts the constraint from market access to execution: its impact on diversification and job creation will be determined less by the agreement itself and more by Nigeria’s capacity to translate access into competitive production and sustained export growth.

FG Doubles January Bond Borrowing to ₦900bn

The Federal Government has doubled its January 2026 bond auction size to ₦900 billion, up from ₦450 billion in January 2025, signaling increased reliance on the domestic debt market early in the fiscal year. The auction comprises reopened medium- and long-dated bonds, including ₦300 billion of the February 2031 bond with an 18.50 percent coupon, ₦400 billion of the February 2034 bond at 19.00 percent, and ₦200 billion of the January 2035 bond carrying a 22.60 percent coupon. Coupon rates represent the fixed interest the government commits to pay investors annually, and in Nigeria’s current market conditions, higher coupons generally translate into higher effective borrowing costs.

Nigeria Opens Sovereign Pavilion at World Economic Forum

Nigeria inaugurated its first sovereign pavilion at the 2026 World Economic Forum in Davos, providing a centralized platform to engage global investors across priority sectors including energy, solid minerals, agriculture, digital services, and the creative economy. The pavilion is designed to improve coordination in Nigeria’s investment messaging and support capital attraction efforts at a time of heightened global risk aversion.

The economic significance of the sovereign pavilion will ultimately depend on post-Davos execution—whether high-level engagements translate into concrete investment commitments, particularly in capital-intensive sectors, and whether domestic policy consistency and regulatory clarity are sufficient to convert investor interest into sustained foreign direct investment.

Nigeria Removed from EU High-Risk Financial List

The National Bureau of Statistics revised Nigeria’s 2025 inflation series upward by approximately 3 percentage points across all months from January to November, following a methodological normalization in the December 2025 Consumer Price Index report. This adjustment stems from a technical flaw in the January 2025 rebasing exercise, where only December 2024 was rebased to 100 rather than applying a 12-month average for 2024 as international standards require.

The normalization lifted previously reported figures substantially: January moved from 24.48% to 27.61%, while November increased from 14.45% to 17.33%. December 2025 headline inflation came in at 15.15%, down from 17.33% in November and significantly below the 34.80% recorded in December 2024. The correction prevents what would have been an artificial 30% headline print in December 2025 had the flawed methodology persisted.

For monetary policy, the normalized series narrows perceived policy space. The Central Bank of Nigeria now faces inflation readings that remained above 20% until August and above 18% through October, compared to earlier data suggesting faster convergence toward single digits. This constrains the timeline for potential rate cuts despite softening real-economy conditions.

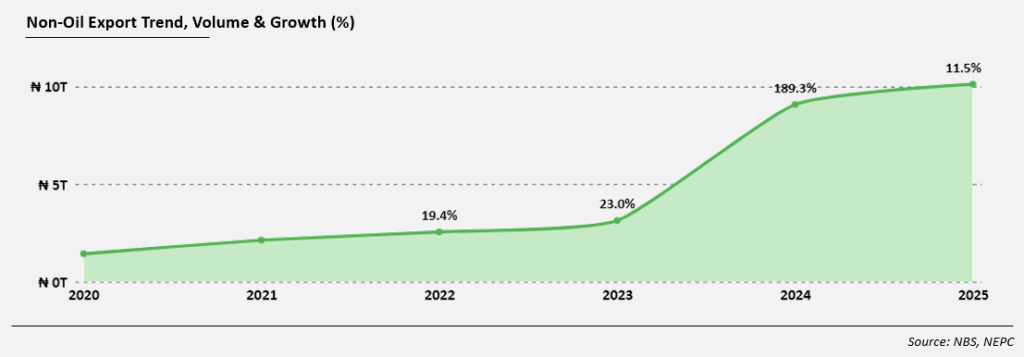

Nigeria’s Non-Oil Exports Reach Historic ₦10.14 trillion in 2025

Nigeria’s non-oil exports rose to a record $6.1 billion (₦10.14 trillion) in 2025, representing an 11.5% increase from $5.4 billion (₦9.09 trillion) recorded in 2024, according to preliminary disclosures by the Nigerian Export Promotion Council (NEPC). The Council described the outcome as the highest formally documented non-oil export value in nearly five decades, supported by stronger performance across agricultural commodities, processed and semi-processed goods, industrial inputs, and solid minerals. Export volumes also increased to 8.02 million metric tonnes, up from 7.29 million metric tonnes in 2024, alongside broader product coverage spanning 281 non-oil export items.

In dollar terms, the increase from $5.4 billion to $6.1 billion points to a measurable rise in external receipts, even as exchange-rate conditions remained volatile. Part of the reported improvement reflects changes in export composition, notably the inclusion of refined petroleum and petrochemical products following the commencement of operations at the Dangote Refinery, which shifted Nigeria toward net exports of select refined products in 2025. While this development broadens the non-oil export base and supports FX inflows, it also complicates year-on-year comparisons, as value gains may reflect product substitution and pricing effects alongside underlying volume growth. A clearer assessment of real export expansion will depend on the release of detailed trade data disaggregating volumes, prices, and product categories.

Nigeria Signs Comprehensive Economic Partnership Agreement (CEPA) with UAE

Nigeria has signed a Comprehensive Economic Partnership Agreement (CEPA) with the United Arab Emirates, deepening bilateral trade and investment ties and establishing a structured framework for goods, services, and capital flows. The agreement comes against the backdrop of a growing Nigeria–UAE trade relationship, with bilateral trade exceeding $4.3 billion in 2024, and reflects Nigeria’s broader efforts to diversify trade partners and reduce reliance on hydrocarbons.

Under the agreement, the UAE will eliminate tariffs on over 7,000 Nigerian products, granting immediate duty-free access for agricultural and industrial exports such as fish and seafood, oilseeds, cereals, cotton, pharmaceuticals, and chemicals. Tariffs on Nigerian machinery, vehicles, electrical equipment, apparel, and furniture will be phased out over three to five years, improving the competitiveness of value-added exports into one of the world’s major trade and logistics hubs. On Nigeria’s side, tariffs will be removed on roughly 6,000 UAE products, with about 60 percent eliminated immediately and the remainder phased out over five years, largely concentrated in capital goods, machinery, and industrial inputs, while the Import Prohibition List remains intact.

Beyond trade in goods, CEPA introduces important mobility and services provisions. Nigerian business visitors will be able to enter the UAE for up to 90 days within a 12-month period to explore commercial opportunities, while intra-corporate transferees, including managers and specialists, can relocate for renewable three-year terms. Nigeria has also made services commitments across 99 service lines in 10 sectors, including financial services, transport, construction, communications, and tourism, which could gradually support services exports and professional mobility.

From a macroeconomic perspective, CEPA strengthens Nigeria’s external position by expanding market access for non-oil exports and improving the attractiveness of the country to long-term investment in logistics, energy, and manufacturing. However, its short-term effect on trade balances will depend on how quickly domestic producers can scale output and meet export standards, as tariff liberalisation also raises the risk of higher imports. The agreement therefore shifts the constraint from market access to execution: its impact on diversification and job creation will be determined less by the agreement itself and more by Nigeria’s capacity to translate access into competitive production and sustained export growth.

FG Doubles January Bond Borrowing to ₦900bn

The Federal Government has doubled its January 2026 bond auction size to ₦900 billion, up from ₦450 billion in January 2025, signaling increased reliance on the domestic debt market early in the fiscal year. The auction comprises reopened medium- and long-dated bonds, including ₦300 billion of the February 2031 bond with an 18.50 percent coupon, ₦400 billion of the February 2034 bond at 19.00 percent, and ₦200 billion of the January 2035 bond carrying a 22.60 percent coupon. Coupon rates represent the fixed interest the government commits to pay investors annually, and in Nigeria’s current market conditions, higher coupons generally translate into higher effective borrowing costs.

Nigeria Opens Sovereign Pavilion at World Economic Forum

Nigeria inaugurated its first sovereign pavilion at the 2026 World Economic Forum in Davos, providing a centralized platform to engage global investors across priority sectors including energy, solid minerals, agriculture, digital services, and the creative economy. The pavilion is designed to improve coordination in Nigeria’s investment messaging and support capital attraction efforts at a time of heightened global risk aversion.

This is particularly relevant given the structure of recent capital inflows. In December 2025, foreign portfolio investment into Nigeria stood at about $632 million, while foreign direct investment amounted to roughly $50 million, underscoring the continued dominance of short-term portfolio flows over long-term productive capital. Although portfolio inflows support near-term FX liquidity, their volatility contrasts sharply with the scale and stability of direct investment needed to finance infrastructure, industrial expansion, and job creation. In this context, Nigeria’s presence at Davos serves as a channel to reposition the country toward attracting larger, more durable FDI inflows that can strengthen external balances and reduce reliance on cyclical portfolio capital.

The economic significance of the sovereign pavilion will ultimately depend on post-Davos execution—whether high-level engagements translate into concrete investment commitments, particularly in capital-intensive sectors, and whether domestic policy consistency and regulatory clarity are sufficient to convert investor interest into sustained foreign direct investment.

Nigeria Removed from EU High-Risk Financial List

The European Union has removed Nigeria from its list of high-risk jurisdictions for money laundering and terrorism financing, lifting enhanced due-diligence requirements on Nigeria-related transactions by EU financial institutions from late January 2026. The decision reduces compliance frictions that had raised transaction costs, delayed payments, and constrained correspondent banking relationships between Nigerian institutions and their European counterparts. In practical terms, the move should ease cross-border trade settlements, support access to trade finance, and improve the efficiency of payments for exporters, banks, and fintechs operating within EU-linked financial corridors.

The EU decision follows Nigeria’s exit from the Financial Action Task Force grey list in 2025 and reflects progress in strengthening anti-money-laundering and counter-terrorism financing frameworks. Beyond Europe, the delisting carries broader signalling value for international financial institutions and global counterparties, as EU risk classifications often influence internal compliance policies across jurisdictions. Sustaining these benefits will depend on continued enforcement of financial integrity reforms and complementary macro stability, as reputational upgrades alone are unlikely to materially lower financing costs or expand cross-border activity without parallel improvements in FX liquidity, trade capacity, and export competitiveness.

Nigeria’s CPI Normalization: Statistical Recalibration, Not Economic Reversal

The National Bureau of Statistics revised Nigeria’s 2025 inflation series upward by approximately 3 percentage points across all months from January to November, following a methodological normalization in the December 2025 Consumer Price Index report. This adjustment stems from a technical flaw in the January 2025 rebasing exercise, where only December 2024 was rebased to 100 rather than applying a 12-month average for 2024 as international standards require.

The normalization lifted previously reported figures substantially: January moved from 24.48% to 27.61%, while November increased from 14.45% to 17.33%. December 2025 headline inflation came in at 15.15%, down from 17.33% in November and significantly below the 34.80% recorded in December 2024. The correction prevents what would have been an artificial 30% headline print in December 2025 had the flawed methodology persisted.

Critically, the normalization does not alter Nigeria’s underlying disinflation trend. Month-on-month dynamics and the trajectory of price moderation remain unchanged—the level shifted upward, but the slope of decline is identical across both series. This indicates that monetary tightening, exchange rate stabilization, and easing food prices did compress inflationary pressures through 2025, though the magnitude of improvement was overstated in initial reports.

For monetary policy, the normalized series narrows perceived policy space. The Central Bank of Nigeria now faces inflation readings that remained above 20% until August and above 18% through October, compared to earlier data suggesting faster convergence toward single digits. This constrains the timeline for potential rate cuts despite softening real-economy conditions.

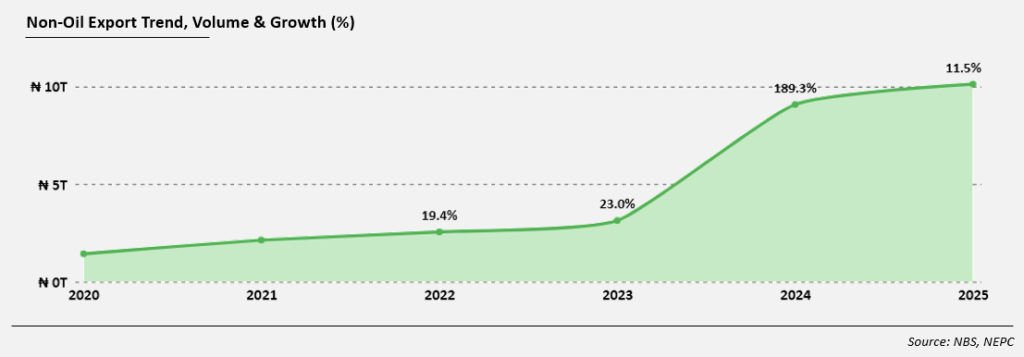

Nigeria’s Non-Oil Exports Reach Historic ₦10.14 trillion in 2025

Nigeria’s non-oil exports rose to a record $6.1 billion (₦10.14 trillion) in 2025, representing an 11.5% increase from $5.4 billion (₦9.09 trillion) recorded in 2024, according to preliminary disclosures by the Nigerian Export Promotion Council (NEPC). The Council described the outcome as the highest formally documented non-oil export value in nearly five decades, supported by stronger performance across agricultural commodities, processed and semi-processed goods, industrial inputs, and solid minerals. Export volumes also increased to 8.02 million metric tonnes, up from 7.29 million metric tonnes in 2024, alongside broader product coverage spanning 281 non-oil export items.

In dollar terms, the increase from $5.4 billion to $6.1 billion points to a measurable rise in external receipts, even as exchange-rate conditions remained volatile. Part of the reported improvement reflects changes in export composition, notably the inclusion of refined petroleum and petrochemical products following the commencement of operations at the Dangote Refinery, which shifted Nigeria toward net exports of select refined products in 2025. While this development broadens the non-oil export base and supports FX inflows, it also complicates year-on-year comparisons, as value gains may reflect product substitution and pricing effects alongside underlying volume growth. A clearer assessment of real export expansion will depend on the release of detailed trade data disaggregating volumes, prices, and product categories.