MONTHLY ECONOMIC UPDATES – FEBRUARY 2026 (NIGERIA, KENYA, AND GHANA)

Executive Summary

February 2026 marked a month of constrained disinflation, asymmetric monetary easing, and mounting geopolitical exposure across the three economies under review. All three countries recorded headline inflation at or near multi-year lows, yet the macro picture diverges sharply beneath the aggregate: Nigeria continues to operate with structurally elevated core inflation and an oil-revenue paradox; Kenya is threading a policy needle between growth stimulation and exchange-rate defense; and Ghana is harvesting a rare combination of macro stabilization and commodity tailwinds, though its gains remain vulnerable to the same geopolitical shock driving them.

The escalating US-Israel-Iran conflict, which drove Brent crude to a multi-year peak of US$118/bbl before settling near US$79-80/bbl, and gold prices to a record US$5,426/oz, is the defining external variable of the period. The conflict reconfigures each country’s risk calculus differently: for Nigeria, higher oil prices offer fiscal upside that production constraints cannot fully capture while inflation and FPI risks intensify; for Kenya, the primary exposure is import-cost pressure on an already managed inflation trajectory; for Ghana, surging gold prices provide an external buffer boost that partially offsets rising fuel and shipping costs.

Pre-election dynamics in Nigeria and Kenya, and Ghana’s growth imperative following its IMF-anchored stabilization, are beginning to shape policy choices. The region’s central banks are all in easing mode, but the pace and durability of that easing now depends as much on geopolitical developments as on domestic fundamentals.

Three economies are at different stages of the same cycle, with disinflation achieved and easing begun, but geopolitical headwinds and electoral pressures now threaten the trajectory.

Geopolitical Context: The US-Israel-Iran Conflict

Energy Price Impact and Regional Macro Transmission

The US-Israel-Iran conflict entered a more intense phase in late February and early March 2026, triggering a sharp repricing across global energy and commodity markets. Brent crude surged to $118/bbl before retreating to approximately $80-92/bbl following President Trump’s remarks signaling a near-term end to hostilities and G7 deliberations over releasing up to 400 million barrels from strategic reserves. Gold simultaneously surged to a record US$5,100/oz, driven by safe-haven demand and systemic uncertainty.

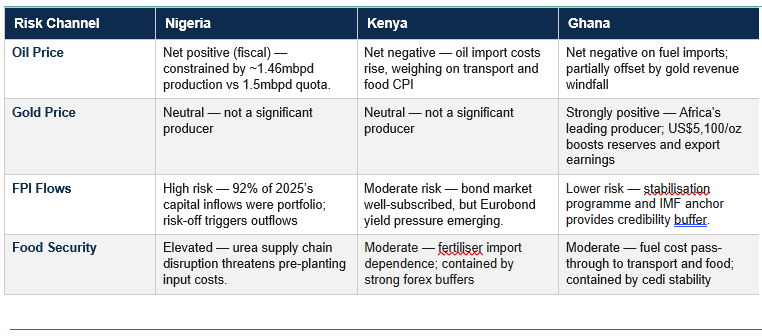

For Sub-Saharan Africa’s three most economically significant Anglophone markets, the conflict creates an asymmetric shock matrix. Nigeria, as an oil exporter, has a theoretical fiscal upside from elevated Brent, but chronic production underperformance limits its ability to translate price gains into government revenues. Kenya and Ghana are both net oil importers, but Ghana’s status as Africa’s leading gold producer means the same risk-off dynamic generating energy cost pressures also delivers a reserve and export earnings windfall.

Strait of Hormuz: Systemic Risk Channel

The Strait of Hormuz, through which an estimated 20% of global oil supply and a substantial share of Qatar’s LNG exports transit, remains the fulcrum of systemic risk. A sustained restriction or closure, whether through direct military action, a naval blockade, or disruption of shipping insurance would constitute a supply shock of the first order. For Nigeria, the upside to LNG exports from such a scenario is structurally constrained by the same Niger Delta infrastructure vulnerabilities that afflict crude output. For Kenya and Ghana, continued disruption along the Strait of Hormuz would predominantly register as an import cost shock, with downstream inflationary effects on transport, food, and manufactured goods.

Geopolitics Exposure Differential

Regional Overview

February 2026: Three-Country Macro Snapshot

Disinflation: The Common Thread

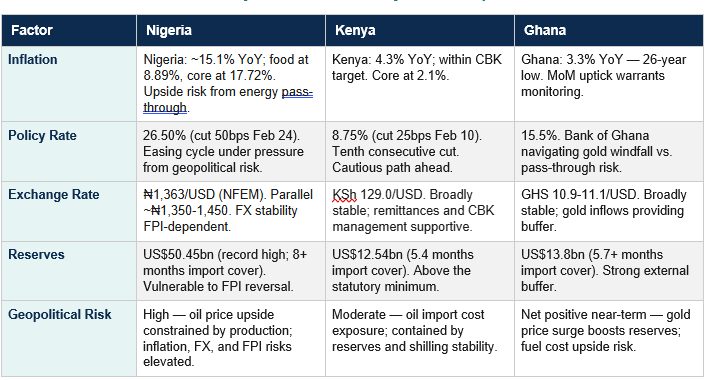

All three economies recorded headline inflation at or near structural lows in February 2026, representing the most significant region-wide disinflationary episode in over a decade. Nigeria’s headline CPI stood at 15.10% YoY, the tenth consecutive monthly decline and down from 29.63% twelve months prior. Kenya’s inflation held at 4.3% YoY, comfortably within the CBK’s 2.5-7.5% target band. Ghana’s 3.3% YoY reading, the 14th consecutive

monthly decline, was the lowest recorded since August 1999. The convergence reflects the lagged impact of coordinated monetary tightening cycles across all three central banks between 2022 and 2024, normalizing global supply chains, favorable food prices, and base effects.

Monetary Easing: Underway but Conditioned

All three central banks are now in an easing cycle, but the pace and room for manoeuvre vary considerably. Nigeria’s CBN cut 50bps to 26.50% in February, the second cut in six months, supported unanimously by all MPC members. Kenya’s CBK cut 25bps to 8.75%, its tenth consecutive reduction. Ghana’s Bank of Ghana is on an implicit easing trajectory, with 91-day Treasury bill yields at 11-12% and lending rates declining toward 19-20%. In each case, however, the geopolitical environment introduces an upside risk to inflation that may compress the space for further easing, particularly if Brent stabilizes above US$80/bbl and fuel cost pass-through accelerates.

Fiscal Pressures and Revenue Constraints

Despite improving macro fundamentals, all three governments face significant fiscal constraints. Nigeria’s 2026 budget assumed oil at US$64/bbl and production of 2.06mbpd, both assumptions are challenged by output underperformance and the structural debt service obligations on NNPCL. Kenya continues to manage debt service costs that absorb a material share of fiscal revenues, amid persistent pressure on the current account deficit. Ghana, while benefiting from the IMF-anchored Domestic Debt Exchange Programme and elevated gold revenues, must demonstrate sustained primary surplus delivery to unlock the remaining tranches of its US$3 billion IMF programme. In all three cases, the fiscal dividend from positive macro dynamics remains contingent on structural reforms that are proceeding unevenly.

Electoral and Political Economy Dynamics

The political calendar is a material input to macro policy assessment across the region. Nigeria faces presidential elections in January 2027, with INEC-mandated party primaries by May 2026, placing the Tinubu administration squarely inside an active electoral cycle. The temptation to accommodate fiscal expansion, resist pump price adjustments, or pressure the CBN on rates will intensify as primaries approach. In Kenya, the August 2027 general elections are already shaping fiscal spending priorities, with the Ruto administration under pressure to deliver on its bottom-up economic model. Ghana’s December 2024 election resulted in a change of government, with the newly installed Mahama administration inheriting the IMF programme and prioritizing growth restoration, a mandate that argues for continued but fiscally prudent stimulus.

Nigeria

Inflation

Nigeria’s headline inflation continued its sustained deceleration, falling to 15.10% YoY in January 2026, the tenth consecutive monthly decline and a 14.53 percentage point reduction from the 29.63% recorded in January 2025. On a month-on-month basis, headline inflation declined to –2.88% in January 2026, compared to 0.54% in December 2025, representing a 3.42 percentage point decline and indicating a sharp improvement in short-term price dynamics beyond base effects.

Food inflation eased to 8.89% YoY, the first single-digit reading in over a decade, driven by lower prices for yams, eggs, grains, palm oil, and cassava. Monthly food deflation of 6.02% (vs. +0.36% in December 2025) suggests supply-side normalization is running ahead of demand recovery. Core inflation at 17.72% YoY remains the most resilient component, reflecting persistent service-sector and structural cost pressures that monetary tightening alone cannot quickly resolve. The gap between headline and core signals that food-price deflation is driving the headline figure while underlying demand-side pressures remain elevated.

Food price deflation is outpacing core disinflation, a structurally significant milestone but one that does not yet signal broad-based price stability across the economy.

Monetary Policy

The CBN’s MPC cut the Monetary Policy Rate by 50 basis points to 26.50% at its February 24, 2026, meeting, the second cut in six months. Governor Cardoso framed the decision as a recognition that eleven consecutive months of declining inflation have sufficiently anchored expectations, creating space for gradual easing to support credit expansion and real sector growth.

The asymmetric corridor remains at +50/-450 basis points. The Cash Reserve Ratio is unchanged at 45.0% for commercial banks and 16.0% for merchant banks, with the Liquidity Ratio at 30.0%. The deliberate tightness of these parameters signals that the CBN is managing a narrow easing corridor by reducing headline policy rates while maintaining structural liquidity constraints to prevent premature credit loosening.

FX and External Reserves

The naira maintained broad stability through February 2026, trading below ₦1,400/USD since January 29 and closing at ₦1,363/USD at the NFEM on February 27, an appreciation of approximately 4.68% over two months. Gross external reserves reached a record US$50.45 billion by February 16, providing over eight months of import cover, up from US$46.1 billion in January. In the parallel market, rates traded within the ₦1,350-1,450/USD range, with the compressed official-parallel spread reflecting improved FX market credibility. This trajectory was reversed in early March due to geopolitical dynamics, with the naira depreciating to about ₦1,410/USD.

The structural vulnerability in Nigeria’s FX position remains acute: portfolio inflows accounted for 85% of total capital inflows in the first nine months of 2025 and 53% of January 2026 FX supply. This carry-trade-dependent stability is inherently reversible. A risk-off rotation driven by the US-Israel-Iran conflict or by any deterioration in the CBN’s reform credibility could trigger rapid FPI outflows that overwhelm the spot market’s intervention capacity. The BDC re-entry into the official FX market, capped at US$150,000/week per operator, has seen limited uptake, with compliance conditions tempering early participation.

Oil Sector and Fiscal Position

OPEC direct communication data placed Nigeria’s crude output at approximately 1.314mbpd in February 2026 — down 9.9% from 1.459mbpd in January, which is below the 1.5mbpd OPEC quota and materially short of the 2.06mbpd embedded in the 2026 national budget. Pipeline vandalism, oil theft, and ageing infrastructure in the Niger Delta continue to cap production recovery.

Brent’s price surge toward $90/bbl, driven by geopolitical risk, provides near-term upside against the budget’s $64/bbl oil price assumption. However, the fiscal dividend is significantly discounted: the country’s inability to produce at quota means higher prices do not translate proportionately into higher federation revenues. Furthermore, NNPCL’s pre-existing debt service obligations, accumulated through subsidy funding, refinery rehabilitation, and joint venture cash call arrears, reduce the share of incremental oil revenues that reach the Federation Account. Project Gazelle collateralization arrangements further subordinate some future crude streams.

Private Sector Activity

Nigeria’s private sector returned to expansion in February 2026. The Stanbic IBTC PMI rose to 53.2 from 49.7 in January, driven by a recovery in new orders (55.5 vs. 49.9) and output (55.8 vs. 50.2) across all four surveyed sectors. The rebound suggests that the combination of naira stability, easing monetary conditions, and lower food price inflation is beginning to support real sector confidence, though the PMI remains sensitive to the unfolding energy price trajectory through the distribution chain.

Near-Term Outlook

Nigeria’s macro trajectory for Q2 2026 will be shaped by three intersecting variables: the durability of the naira’s stability under FPI outflow pressure; the extent to which Dangote Petroleum Refinery gantry price increases pass through to retail pump prices and headline inflation; and whether the 2027 electoral cycle begins to shape fiscal spending patterns.

- Inflation is expected to rise modestly from its January 2026 base, as higher fuel prices could push up food and transport prices. The MPR at 26.50% provides some room for the CBN to hold off on increasing rates, but a sustained energy-driven inflationary uptick will reduce the space for further near-term cuts.

- FX stability remains a critical variable. Reserves are at a record high, but sustained global tensions, which are currently driving a flight-to-safety sentiment from emerging markets by investors, could lead to an outflow of portfolio investments, which has been critical in shaping the stability of the naira.

- With party primaries due by May 2026, the government’s appetite for politically costly policy adjustments, including market-driven fuel price dynamics, could diminish. ACIOE assesses a moderate and rising risk that electoral considerations will begin to influence spending priorities and the pace of structural reform delivery.

- The oil sector upside is real but capped. Sustained Brent prices above $80/bbl will help to marginally reduce the fiscal deficit; however, significant gains would depend on improved output exceeding 1.5 mbpd.

Kenya

Inflation

Kenya’s inflation profile remained the most contained of the three economies under review. Headline CPI eased marginally to 4.3% YoY in February 2026, from 4.4% in January, comfortably within the CBK’s 2.5-7.5% statutory target band. Month-on-month inflation stood at 0.6%, driven by food and transport costs, the two channels most directly exposed to global energy price transmission.

Food and non-alcoholic beverages inflation at approximately 7.8% YoY remains the primary upside risk within an otherwise contained CPI basket. Core inflation fell further to 2.1% from 2.2% in January as transport and utility prices eased, indicating that domestically generated price pressures are well-anchored. The risk, however, is that rising global oil prices feed back into Kenyan transport costs, a direct CPI input, potentially testing the CBK’s confidence that inflation will remain within target through the rest of 2026.

Monetary Policy

The CBK’s Monetary Policy Committee lowered the Central Bank Rate by 25 basis points to 8.75% at its February 10, 2026, meeting, the tenth consecutive reduction from a peak of 13.0% in February 2024. The decision reflected the MPC’s assessment that contained price pressures provide space to support private sector credit and broader economic activity, while exchange rate stability remains intact.

The cautious 25bps increment, against Nigeria’s 50bps and Ghana’s implicit trajectory, reflects the CBK’s balancing act: inflation is at the lower half of the target band, but the external environment is now more uncertain than at any point since the easing cycle began. The CBK faces the specific challenge that Kenya’s oil import bill is directly sensitive to Brent price movements, creating a potential inflation re-acceleration scenario that would require the easing cycle to pause or reverse.

Exchange Rate and External Position

The Kenyan shilling maintained broad stability throughout February, with the average rate of approximately KSh 129.0/USD showing negligible movement. The currency closed at KSh 129.03/USD on February 26. Exchange rate management was supported by steady export earnings, diaspora remittances, Kenya’s most reliable FX inflow source, and active CBK market intervention.

Gross FX reserves stood at US$12.535 billion as of February 26, equivalent to 5.4 months of import cover, 35% above the CBK’s statutory four-month minimum and sufficient to absorb near-term external shocks. Money market conditions were liquid, with commercial banks holding excess reserves of KSh 52.3 billion above the 3.25% CRR requirement as of February 26.

Fixed Income and Capital Market Conditions

Kenya’s government securities market demonstrated exceptional depth in February. Treasury bill auctions recorded subscription rates of 243.9% to 308.8% against an advertised KSh 24.0 billion per auction, with the February 26 auction attracting total bids of KSh 58.5 billion. The 15-year and 25-year Treasury bond reopenings attracted bids of KSh 213.8 billion against an advertised KSh 50.0 billion, a 427.5% subscription rate, reflecting deep investor appetite for longer-dated government paper.

Secondary bond market turnover rose consistently through the month: up 2.08%, then 57.21%, and a further 36.9% in the final week. Eurobond yields increased by an average of 8.44 basis points during February before easing to +1.68 basis points by month-end, suggesting that the initial geopolitical risk repricing was partially absorbed. The trajectory of Kenya’s Eurobond yields in March will be a key indicator of international investor sentiment toward the credit.

Near-Term Outlook

Kenya enters Q2 2026 with a strong set of macro fundamentals, but faces a more complex external environment than at any point in its current easing cycle. The primary risks are oil-driven: if Brent sustains above $80/bbl and the cost passes into domestic fuel prices, transport inflation could push food and headline CPI toward the upper end of the target band, compressing the CBK’s room for further cuts.

- The tenth consecutive rate cut positions Kenya as the region’s most advanced easing cycle. The pace of further reductions will depend on inflation performance, the shilling’s exchange rate trajectory, and developments in the Eurobond market through Q2 2026.

- Kenya’s bond market over-subscription signals strong domestic and international appetite for government paper, which supports fiscal financing. However, it also concentrates sovereign risk in an environment where a geopolitical shock could trigger an abrupt reassessment of frontier-market exposure.

- The pre-election environment, with general elections due in August 2027, is beginning to condition fiscal posture. The Ruto administration’s bottom-up economic agenda requires visible delivery, creating incentives for spending acceleration that may test the consolidation narrative.

- Kenya’s diaspora remittance inflows and diversified export base (tea, coffee, horticulture, services) provide a more resilient FX position than Nigeria’s FPI-dependent model, an important structural advantage in a risk-off environment.

Ghana

Inflation

Ghana’s disinflationary momentum accelerated in February 2026, with headline inflation declining to 3.3% YoY from 3.8% in January, the 14th consecutive monthly decline and the lowest reading since August 1999. The achievement is analytically significant: Ghana’s inflation peaked at 54.1% in December 2022, at the height of the economic crisis, making the 50.8 percentage-point decline over 38 months one of the most rapid disinflationary episodes in sub-Saharan African economic history.

Food inflation fell sharply to 2.4% YoY from 3.9% in January, while non-food inflation edged marginally higher to 4.0% from 3.9%, suggesting that the disinflation is primarily supply-driven and that service-sector and cost-push pressures remain modest but present. The 0.8% month-on-month increase (vs. 0.2% in January) warrants monitoring: while consistent with seasonal adjustment, a sustained MoM acceleration from these levels would indicate that the headline disinflation trend is beginning to exhaust its impulse.

Ghana’s inflation at 3.3% YoY in February 2026 represents one of the most rapid disinflationary recoveries in sub-Saharan Africa’s recent economic history, achieved within 38 months of a 54.1% peak.

Monetary and Financial Conditions

Money market rates continued their orderly downward adjustment in February. The 91-day Treasury bill yield stabilised near 11-12%, while average lending rates moderated toward 19-20%, a real rate environment that remains positive and supportive of financial sector stability. Real private-sector credit growth of approximately 13% in the double digits indicates that the monetary transmission mechanism is functioning and that demand for credit is recovering, consistent with an economy exiting a stabilisation phase.

Bank of Ghana maintained disciplined open market operations through the month, supporting liquidity management without injecting inflationary stimulus. The central bank is navigating a narrow path: the gold-driven improvement in the external position argues for continued easing, but the month-on-month inflation uptick and rising global fuel costs argue for caution. ACIOE anticipates that the Bank of Ghana will maintain a gradual easing bias through Q2 2026, subject to maintaining the IMF programme’s primary surplus target.

External Sector: The Gold Windfall

Global gold prices surged to a record US$5,426/oz in February 2026, up approximately 25% in the month, driven by safe-haven demand from the US-Israel-Iran conflict, a weaker US dollar, and structural central bank buying that has underpinned the bull market since 2022. For Ghana, as Africa’s leading gold producer, this represents a substantial and immediate boost to export earnings, fiscal revenues through royalties and corporate taxes on mining operations, and gross international reserves.

Gross international reserves held close to US$13.8 billion, equivalent to above 5.7 months of import cover, among the strongest reserve positions in the region. The cedi remained broadly stable within the GHS 10.9-11.1/USD range, supported by gold inflows, ongoing cocoa receipts, and prudent liquidity management. The currency’s stability is a material achievement given that the cedi depreciated approximately 50% against the dollar during the 2022 crisis.

The geopolitical risk creating the gold windfall simultaneously threatens to push up fuel and shipping costs — with potential inflationary pass-through into food, transport, and manufactured goods. This dual exposure is the defining tension in Ghana’s near-term outlook: the same global shock that boosts external revenues also introduces an upside inflation risk that could moderate the pace of Bank of Ghana easing.

IMF Programme and Fiscal Position

Ghana’s macroeconomic stabilisation remains anchored by its US$3 billion IMF Extended Credit Facility, secured in May 2023 following the Domestic Debt Exchange Programme. The programme has provided the fiscal framework, discipline, and external credibility that enabled the disinflationary recovery. With the Mahama administration entering its first full year in office, programme compliance, including the delivery of the primary surplus and the completion of external debt restructuring, remains the central determinant of Ghana’s macro credibility and market access.

Near-Term Outlook

Ghana’s macroeconomic position in February 2026 is the strongest it has been since the 2022 crisis, and the gold price windfall provides an additional buffer. However, the durability of the current trajectory depends on maintaining IMF programme discipline while executing the Mahama government’s growth mandate, a combination that requires careful sequencing of fiscal and monetary policy.

- Gold prices at US$5,426/oz represent a structural tailwind for Ghana’s external position and fiscal revenues. A sustained price above US$4,500/oz would accelerate reserve accumulation and could reduce Ghana’s reliance on concessional financing, a medium-term positive for debt sustainability.

- The month-on-month CPI uptick of 0.8% in February, against 0.2% in January, warrants close monitoring. If fuel cost pass-through from rising Brent prices feeds into a sustained MoM acceleration, the Bank of Ghana may need to pause its implicit easing trajectory to defend the disinflation achievement.

- Ghana’s IMF programme review calendar will be the key fiscal signpost for Q2 2026. Successful completion of the next review, expected mid-year, would unlock additional disbursements and reinforce market confidence in the post-crisis stabilisation narrative.

- The new Mahama administration’s growth imperative creates political economy pressure for fiscal expansion. ACIOE assesses that this pressure will be managed within IMF programme constraints in the near term, but it will require monitoring as the government seeks to establish its delivery credentials.

Conclusion

February 2026 captured a moment of regional macro achievement, simultaneous disinflation across three major economies, easing monetary cycles in all three central banks, and historically strong external reserve positions. The achievement is real and policy-driven: the tightening cycles of 2022-2024 have delivered their intended disinflationary outcomes, and the sequenced easing now underway represents a broadly competent regional monetary policy response.

The durability of this position, however, faces its most significant external test since the recovery began. The US-Israel-Iran conflict has reshuffled the macro risk deck asymmetrically across the three economies. Nigeria bears the highest net risk exposure. Its oil-revenue paradox (theoretical upside constrained by structural production underperformance), FPI-dependent FX stability, and rapidly approaching electoral cycle combine to create a policy environment where the margin for error is narrow, and the temptation to accommodate is growing. Kenya’s contained inflation and diversified FX inflow base provide greater resilience, but oil import sensitivity and Eurobond market dynamics demand vigilance. Ghana’s gold windfall provides an exceptional external buffer, but the parallel risk of fuel cost-driven inflation re-acceleration could complicate the Bank of Ghana’s easing path and test the IMF programme’s primary surplus anchors.

The regional macro achievement of February 2026 is built on foundations that are simultaneously strong and fragile: strong because the disinflationary recovery is policy-credible; fragile because the external shock now in motion tests each economy’s structural vulnerabilities with precision.

ACIOE’s central assessment is that the region navigates the next two quarters with broadly stable macro fundamentals, but with a widening divergence in policy latitude: Ghana retains the most room for manoeuvre; Kenya operates on a cautious but credible easing path; Nigeria faces the narrowest policy corridor and the highest political economy risk. The key variables to track are the trajectory of Brent crude through Q2 2026, the durability of Nigeria’s FPI-dependent FX stability, and the extent to which electoral considerations begin to condition fiscal and monetary policy in Abuja.