Monthly Africa Economic Report: May 2026

Nigeria | Ghana | Kenya

ABRIDGED EDITION | Access the Full Report | contactus@acioe.com

Executive Summary

May 2026 marks a decisive inflection in the macroeconomic trajectories of Nigeria, Ghana, and Kenya. The US-Israel-Iran conflict and extended Strait of Hormuz disruption, which defined April’s commodity pricing environment, registered differently across the three economies in May: Murban crude declined to approximately $89.13 per barrel by early May (from highs above $115 in April), offering near-term import relief, but domestic institutional responses to prior-month shocks became the dominant drivers of macro and sector risk. The overarching narrative shifted from reactive stabilisation to contested structural test.

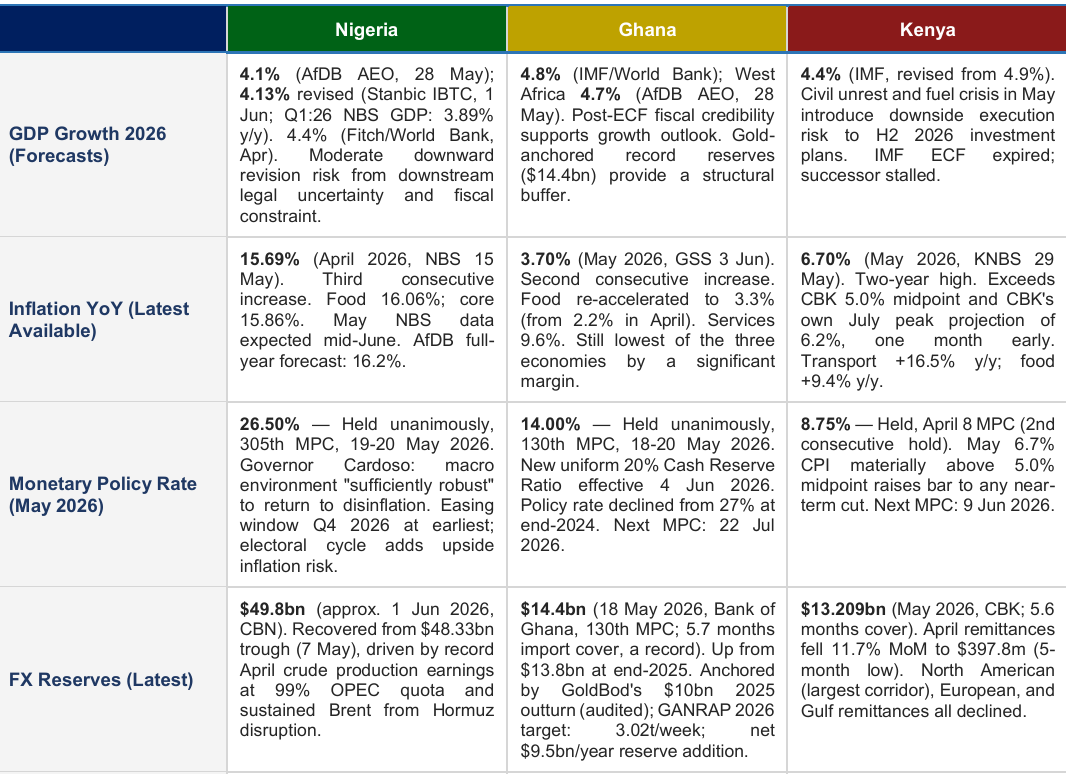

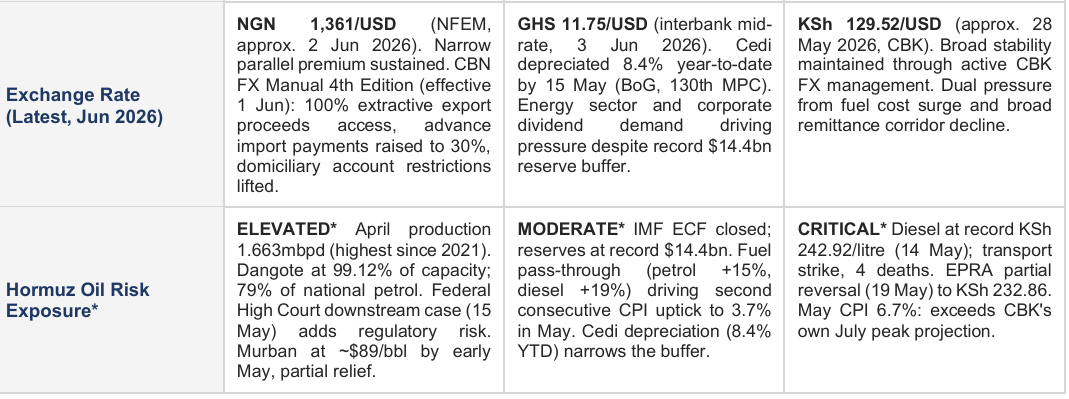

Nigeria delivered its strongest upstream performance since 2021 in April: crude and condensate production reached 1.663 million barrels per day (mbpd), 99 percent of OPEC quota, while the Dangote Petroleum Refinery operated at 99.12 percent of its 650,000 barrels per day nameplate capacity, covering approximately 79 percent of domestic petrol demand. Against these gains, Dangote filed Suit No. FHC/L/CS/857/2026 at the Federal High Court on 15 May, targeting Nigerian Midstream and Downstream Petroleum Regulatory Authority (NMDPRA) fuel import licences; the Nigerian National Petroleum Corporation (NNPC) subsequently filed a counter-affidavit, and NMDPRA applied to join as a formal defendant, transforming a commercial dispute into a statutory interpretation of the Petroleum Industry Act (PIA). External reserves recovered from their $48.33 billion trough of 7 May to approximately $49.8 billion by 1 June, driven by record crude production earnings. The CBN held the Monetary Policy Rate (MPR) at 26.50 percent at the 305th Monetary Policy Committee (MPC) meeting (19-20 May) and launched the 4th Edition Foreign Exchange Manual (effective 1 June), a comprehensive update of Nigeria’s 2023 FX framework. The Stanbic IBTC Nigeria PMI rose to a nine-month high of 54.1 in May.

Ghana completed its most important institutional transition since the 2022 debt crisis: the IMF Extended Credit Facility (ECF) formally closed on 15 May, the sixth review completed ahead of schedule, with a 36-month Policy Coordination Instrument (PCI) agreed. Gross international reserves reached a record $14.4 billion (5.7 months of import cover) as confirmed by Bank of Ghana Governor Dr. Johnson Asiama at the 130th MPC press briefing (20 May). The policy rate was held unanimously at 14.00 percent. The cedi depreciated 8.4 percent year-to-date by mid-May, trading at approximately GHS 11.75 per US dollar as of 3 June. Headline inflation rose for the second consecutive month to 3.7 percent (Ghana Statistical Service, 3 June 2026), with food inflation re-accelerating to 3.3 percent from 2.2 percent in April. The S&P Global Ghana PMI held at exactly 50.0 in May, signaling no net change in private sector conditions.

Kenya faced the most acute domestic disruption. The EPRA fuel price review of 14 May pushed diesel to a record KSh 242.92 per litre, triggering a nationwide transport strike, four deaths, and Mombasa port disruption. EPRA partially reversed diesel to KSh 232.86 on 19 May. Annual inflation surged to 6.7 percent in May (KNBS, 29 May), exceeding the CBK’s own July peak projection of 6.2 percent one month early, with transport costs rising 16.5 percent year-on-year. April remittances fell 11.7 percent month-on-month to $397.8 million, a five-month low, as the US-Israel-Iran conflict depressed earnings across North American, European, and Gulf corridors simultaneously. The CBK held the Central Bank Rate (CBR) at 8.75 percent; the next MPC meeting is 9 June 2026. Kenya’s IMF ECF expired April 2025 and successor negotiations have stalled, leaving Kenya without a sovereign credibility anchor at precisely the point when its fiscal and inflation metrics are under the most pressure.

The Africa Forward Summit (11-12 May, Nairobi) provided a continental policy backdrop: France pledged EUR 23 billion ($27 billion) in investment commitments, the African Development Bank released its 2026 African Economic Outlook (Brazzaville, 28 May) projecting continental growth at 4.2 percent, and President Tinubu used the summit to frame Nigeria’s $11.6 billion annual debt service bill as the structural case for global financial architecture reform.

Regional Overview: May 2026 Country Macro Snapshot

Six core indicators across Nigeria, Ghana, and Kenya. The full 12-indicator table with Debt-to-GDP, Debt Service Pressure, Key Policy/Governance Change, IMF Programme Status, and Primary Opportunity analysis is available in the complete report.

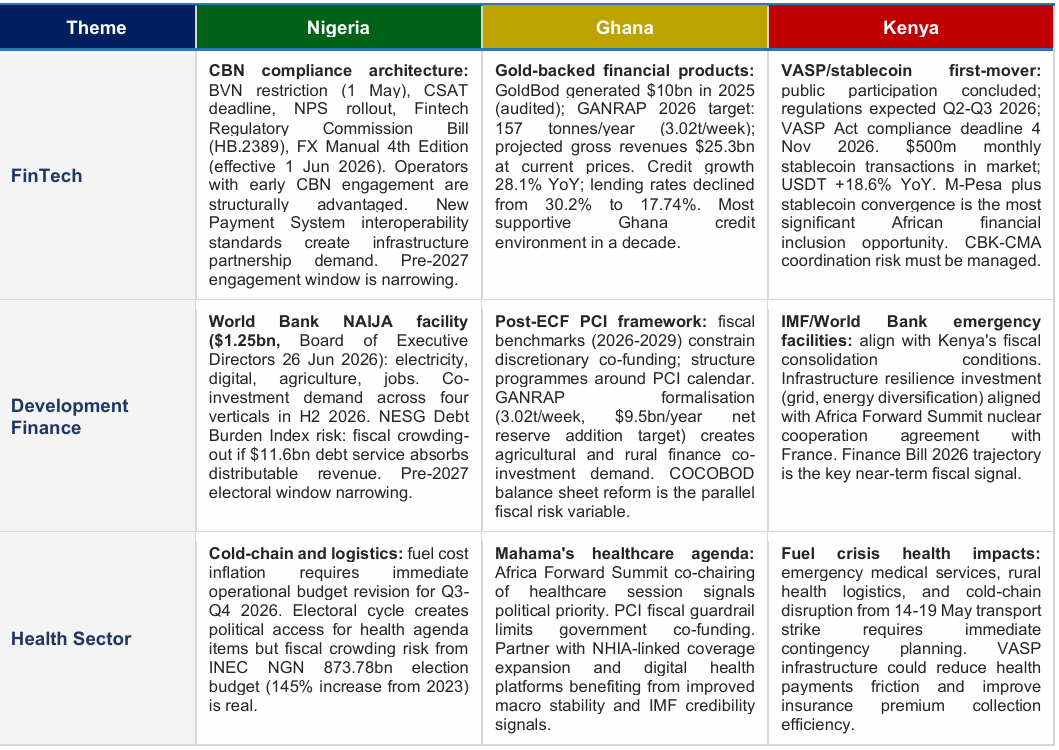

Key Opportunities for Development, Health, and FinTech Partners

Cross-country opportunity assessment for institutional investors, development finance organisations, and sector partners in May-December 2026. Detailed sector spotlights (Financial Services and FinTech, Agriculture and Food Security, Healthcare, Manufacturing) are available in the full report.

ACCESS THE FULL REPORT

This is an abridged edition of the May 2026 Monthly Africa Economic Report by ACIOE Associates. The full report includes comprehensive country-level analysis for Nigeria, Ghana, and Kenya; detailed Geopolitical Risk and Security Profiles; cross-country Sector Spotlights (Financial Services and FinTech, Agriculture and Food Security, Healthcare and Infrastructure, Manufacturing and Exporters); Country Buffers and Sector Opportunities analysis; and a ten-indicator forward-looking Outlook table covering Q2 to Q4 2026.

To receive the complete May 2026 edition and future monthly reports, complete the access request form or contact the ACIOE Public Policy and Government Relations team directly. Request Access via Form or email contactus@acioe.com for subscription, institutional access, and consultation enquiries.